Making the most of a calamity: Case of the Indian IT industry

• The Indian IT services industry is expected to see an adverse impact in the short-term due to COVID-19 outbreak.

• On the demand side, developed economies that contribute to the majority of revenues will see delayed commencement of scheduled new projects, reduced discretionary expenditure as well as overall lower spend owing to sluggish economic growth.

• On the supply side, Indian IT services will face hassles such as travel restrictions to developed countries, closure of offices/work from home and lower discretionary spend by corporates.

• The roadmap for the industry includes increased investments on collaboration tools; more investments on robotics and automation; push for increased onshore and local presence and consolidation of vendors and potential for new partnerships. Companies will also have to be cognizant of sensitive and critical data policies.

With more than 17,000 firms, presence of 75% of global digital talent and over 45% share in Indian services exports in 2018, the Indian IT industry has carved a niche for itself as a one- stop-shop for corporations across the world for their business solutions. This has been the product of favourable policies like up to 100% FDI in data processing, software development and computer consultancy services as well as the country’s cost competitiveness in providing quality IT services.

The National Association of Software and Services Companies (NASSCOM) had opined in February 2020 that India’s information technology and back-office sector is expected to grow by 7.7% in fiscal 2020 to US$ 191 billion, with exports touching US$ 147 billion.

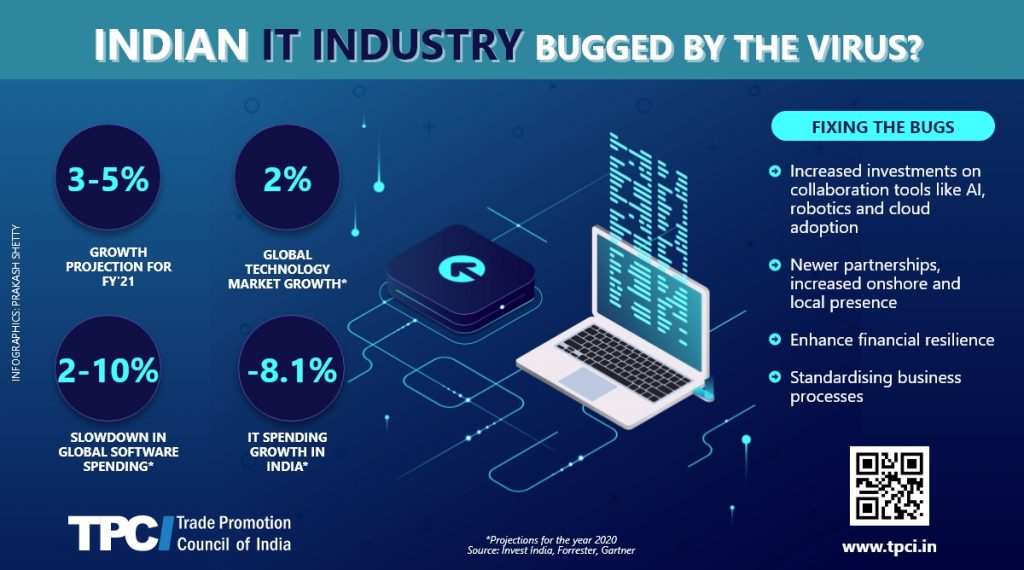

This sanguine outlook preceded the outbreak of the COVID-19 pandemic across the globe. The growth outlook for the sector is now predictably subdued. Ratings agency, ICRA expects the sector to grow at 3-5% in FY 2021, revising its earlier expectation of 6-8%. This forecast, however, is based on the assumption that there will be a gradual recovery during the second half of the year. This bleak growth is attributed to simultaneous supply and demand shocks emerging from the spread of the disease across the world.

On the demand side, delayed off-take of scheduled new projects by developed countries will be a major cause of pain to IT players. Firstly, companies do not want to purchase complicated services without some form of travel and on-field interaction. Second, any major initiatives would require executive support and energy, and they won’t have time to push contracts forward during the next few months. It is also expected that in the coming months, challenges created by the US elections, Brexit, and trade wars will continue to cast a shadow of uncertainty over the sector’s performance in the third and fourth quarters.

Reduced discretionary spend as well as overall lower spend owing to tepid economic growth is another cause of concern. Gaurav Jain, Vice President, ICRA, explains:

“The US and the Euro zone, which generate more than 80% of IT Services export revenues will see their GDP growth fall from 2.3% and 1.2% in CY 2019 to 1.5% and 0.7% respectively in CY 2020.”

Research firm Forrester has predicted that global technology market growth will slowdown to around 2% in 2020. Further, it predicts that technology consulting and systems integration services spending will drop by 5%, software spending growth will slow to the 2-4% range in the best case scenario and computer and communications equipment spending will fall by 5-10% in the second half of the year.

Further, be it travel and hospitality, oil and gas or manufacturing and retail – the virus has created economic hardships everywhere. These sectors are among the worst casualties of the COVID-19 health emergency. As virus continued its unrelenting movement to other countries and travel restrictions around the world have been intensified further, Foreign Tourist Arrivals (FTAs) across the world softened and consequently hotels saw their occupancy rates and earnings decline. In the context of oil, there is a consensus in the industry that its plunging prices are a sign of global markets’ nervousness amid still-evolving impact of the pandemic on global demand and activity. This uncertainty is being reflected in company balance sheets and would weigh on foreign flows in India.

Further, according to a survey by PwC in USA & Mexico, around 54% of CFOs feel that an outbreak puts an impact on their business operations. There are lots of areas where finance leaders showed their apprehensions such as reduction in consumer confidence, plummeting consumption, impact on liquidity and capital resources, reduction in productivity, supply chain issues, and shrinking revenue etc. Lockdowns, factory closures around the world and the halt of production will consequently hurt the manufacturing sector. Meanwhile, as consumers remain locked in their homes, see their incomes dwindling and stick to purchasing just essentials, the retail sector has been dealt a crippling blow too.

On the supply side, travel restrictions will perhaps remain the key challenge. Ratings agency ICRA stated:

“The margins for the Indian IT services are already facing challenging operating environment characterised by continued pressure on commoditised IT services, wage inflation, higher onsite costs necessitated by visa curbs as well as lower discretionary spend by corporate.”

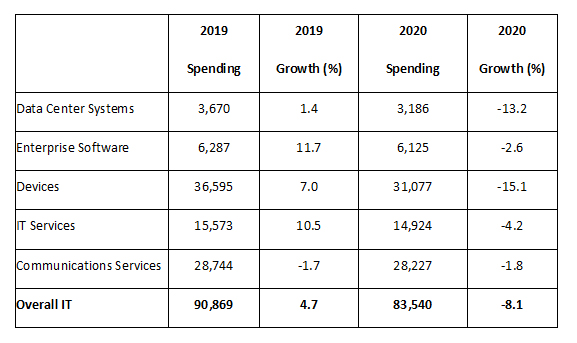

Further, lower discretionary spend by corporates in India is another supply side constraint. According to a recent update by the research firm, Gartner, for the first time in 5 years, IT spending in India is projected to fall by 8.1% in 2020 due to covid-19. The firm predicts that spending on devices and data center systems in India will see the steepest declines in 2020, at -15.1% and -13.2%, respectively.

The firm also opines that in order to maintain government restrictions on social distancing, Indian companies will need to spend more on business continuity, remote working and workforce collaboration. Thus, there will be a shift in spending towards technologies such as desktop as a service (DaaS), infrastructure as a service (IaaS), virtual private network (VPN) and security. Expenditure on enterprise software is set to record a moderate decline in 2020 at -2.6%.

Thus, Naveen Mishra, Gartner’s senior research director, opines, sectors such as retail, insurance, and banking that were already advanced in their digital transformation have to reduce their IT spending in 2020. These sectors will continue to spend on targeted digital initiatives such as artificial intelligence, machine learning and virtual sales assistants, however, they will have to reduce or stop spending on business transformation, process re-engineering and modernization of existing systems.”

India IT spending forecast (US$ million)

Source: Gartner (June 2020)

The closure of offices / work from home will also take a toll on the sector. In a situation where numerous global companies depend on Indian IT sector to run their critical operations and transformational projects, the pandemonium created by coronavirus in India has taken the industry by surprise. This is especially true in the context of smaller companies. For example, British companies receiving business process outsourcing and IT services from India will face disruption. “For many UK businesses, the problems in India risk key functions going offline. That has added to the chaos at many UK operations and delivery centres over the last 24 hours,” according to Andrew McIntee, managing director at New Street Group. He adds that this has resulted in an outpouring demand for employing professionals like business process change specialists, who can help redirect work from India back to the UK. This is indeed a worrying development for industry back home.

Another concern that has emerged pertains to concerns over data security and privacy. IT firms need to take proper security measures to protect sensitive client information and prevent breach of client confidentiality. According to experts, India doesn’t have a data protection law or a dedicated law on cyber security or privacy. Companies should also clearly formulate WFH policies to prevent information from leaking.

D D Mishra, Sr Director Analyst, Gartner, affirms:

“The remote work enablement goes beyond tools and devices. It begins with assessment of organisations’ capacity to enable work from home. It requires assessment of tool, platforms, security, network considerations.”

Going forward, some of the suitable short-term operational adjustments include:

i. Increased investments on collaboration tools:

Customers and IT companies are must gradually scale up their investment significantly on the latest collaboration tools and embracing of new technologies such as 5G networks. They must adopt technologies like AI, robotics and cloud adoption when the revival happens.

ii. Newer partnerships

Companies abroad may push for increased onshore and local presence and consolidation of vendors and potential for new partnerships. Companies will also have to be cognizant of sensitive and critical data policies while drafting these alliances, with the right offshore security protocols.

iii. Enhance financial resilience

Companies may find it prudent to work in collaboration to improve their financial resilience and adopt suitable business models. Adjusting the mix of labor in locations, pushing out payments, or implementing lean transformations could be some strategies to weather the crisis.

iv. Standardising business processes

Uniform business practices across geographies can enable smooth backup of roles, thereby minimising additional staff training at the time of need. Such business continuity solutions would make the industry better equipped for scenarios such as global shutdowns and prolonged disruption.

Leave a comment