Steel industry: Weathering the perfect storm?

The steel industry faced a volatile and rapidly changing market in the first half of 2022, with prices and supply changing hastily due to a variety of factors, including geopolitical conflict, raw material costs and supply chain constraints, apart from the imposition of export duty by the government. Nonetheless, the long term outlook for Indian steel remains stable.

Image credit: Shutterstock

China is one of the world’s largest economies and the global leader in steel production. Currently, China’s economy is struggling following a series of COVID lockdowns in major cities such as Shanghai and Beijing. In April 2022, sentiment among manufacturing and services businesses fell to its lowest level since February 2020, as many businesses were forced to shut down operations to control the spread of COVID cases. China has stated it would enact policies for stimulating growth, including the acceleration of value-added tax refunds and monetary policy changes to encourage positive economic activity.

Europe, which has a major influence on the overall world economy, is experiencing inflation at an all-time high within the Eurozone. The gap between the highest and lowest inflation rates among countries using the Euro has also climbed up in April 2022, indicating economic instability within the region. The war between Russia and Ukraine has already impacted raw material prices and availability. It directly impacts steel supply and the materials used to produce steel. The world is watching closely how things will evolve in the second half of this year.

Growth is expected to return in 2023, but on the strong presumption that the war in Ukraine will come to a conclusion this year and we may see a recovery in market sentiment as we enter into the new year.

Trends in World Steel Production

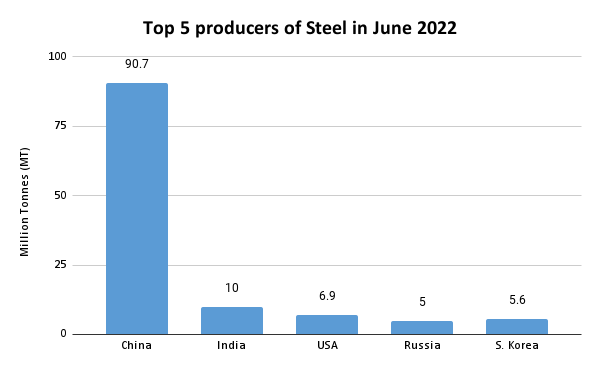

World crude steel production for the 64 countries (reporting to the World Steel Association) was 158.1 million tonnes (Mt) in June 2022, a 5.9% decrease compared to June 2021. As per the World Steel Association data, India is the only country which registered a positive growth in its steel output during June 2022.

- China produced 90.7 MT in June 2022, down 3.3% over its 93.9 MT production in June 2021

- India’s crude steel production increased by over 6% year-on-year to 10 million tonnes in June 2022. It produced 9.4 million tonnes (MT) during June last year, and is the world’s second largest producer of crude steel after China.

- Production of steel in the US fell by 4.2% to 6.9 MT in June from 7.1 MT in the same month of 2021.

- Russia is estimated to have produced 5 MT, down 22.2% as compared to 6.4 MT a year ago. Russia has registered the highest fall among the top 10 steel producers.

- While South Korea registered a 6% fall to 5.6 MT, Germany produced 3.2 MT, down 7% year-on-year.

- In June 2022, Turkey produced 2.9 MT crude steel, down 13.1%, and Brazil is estimated to have produced 2.9 MT, registering a fall of 6.1%.

- Iran is estimated to have produced 2.2 MT, down 10.8%.

Global demand for steel

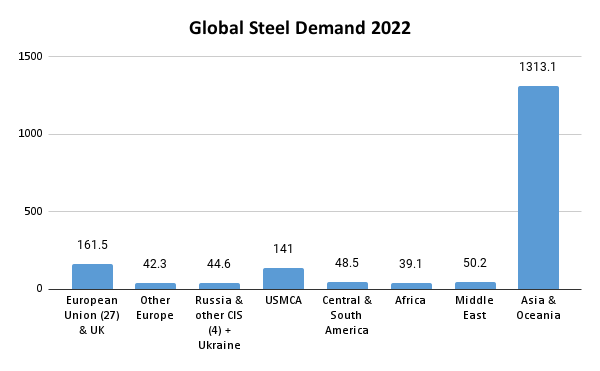

World Steel Association (WSA) Short Range Outlook April 2022 report has projected the global steel demand in 2022 at around 1,840.2Mt. Forecasting a growth rate of 2.2%, global demand for steel is estimated to be 1,881.4Mt for 2023.

WSA has projected a highest steel demand in the Asia and Oceania region at 1313.1 million tonnes for 2022, whereas demand from Africa is estimated at 39.1 million tonnes, the lowest amongst all regions. The graph below shows the demand for steel in various regions as estimated by WSA for \2022.

The eight (8) regions are: European Union (27) & UK, Other Europe, Russia & other CIS (4)+ Ukraine, United States-Mexico-Canada Agreement (USMCA), Central & South America, Africa, Middle East, Asia and Oceania.

Source: WSA

Indian Steel Industry

Steel production in India remained flat on a month-on-month basis in July 2022 at 9.97 mt, down 0.7% year-on-year, after the imposition of export duty on steel in May this year.

Prices of Cold Rolled Coils (CRC) steel declined to Rs 70,915 a tonne in June 2022 from the peak of Rs 85,237 per tonne in April, this year. However in May 2022, when the government announced 15% export duty, steel prices came down to Rs 79,106 per tonne and further to Rs 70,915 a tonne in June 2022. For the month of August, status of CRC, HRC and Rebar prices is as follows:

- Cold-rolled coil (CRCs) prices are further down by ₹2,650/tonne (around 4% month-on-month), now in the Rs. 65,350-66,500 per tonne range for August deliveries.

- Month-on-month prices have declined by 3-4% with Hot Rolled Coil (HRC) prices now being in the range of Rs. 58,000–59,000 per tonne; amongst the lowest so far in 2022,

- Rebar price stood at Rs. 56,900 per tonne, down by 3-4%, month-on-month.

Trends in Indian Steel Exports

Exports of steel have been badly hit since the imposition of a 15% duty in May. A decline in export orders has been seen, consequent to the 15% export levy. Many mills have opted for production cuts in July to restore the supply-demand imbalance, especially in flat steel. Since May, the key markets of West Asia, Europe and Vietnam have seen less bookings for Indian Hot rolled Coil (HRC).

For the April to June quarter, exports declined 39%, year-on-year, falling by 60% in June. India’s finished steel exports fell by 75% y-o-y in July 2022 due to the combined impact of the duty levy, seasonal weakness in demand and global slowdown in the commodity cycle. This was the fourth straight month of fall in exports of Indian steel. Just 1,56,000 tonnes were exported in July.

However, alloyed steel (with no export duty levy) and stainless steel exports defied the trend and saw a 33% rise month-on-month and a 72% leap y-o-y, respectively. According to data from the Ministry, 223,000 tonnes of alloyed/stainless steel exports were recorded in July 2022, compared to 168,000 tonnes in June.

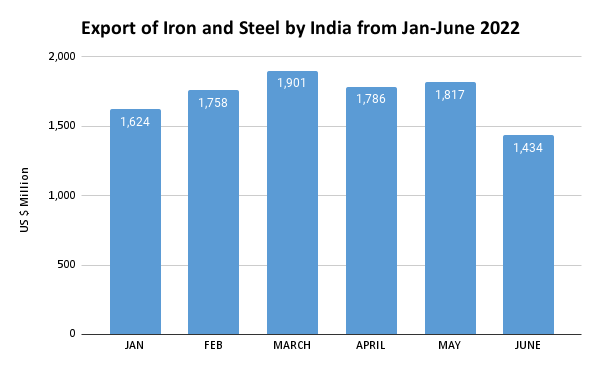

The graph shows the trend in exports of Iron & Steel (HS Code 72) from India in the last six months, from January to June 2022.

| Iron & Steel Exports from India | |

| Month | Exports in US$ million |

| JAN | 1,624 |

| FEB | 1,758 |

| MARCH | 1,901 |

| APRIL | 1,786 |

| MAY | 1,817 |

| JUNE | 1,434 |

Source: MoC & I

Forward outlook

• Steel companies in India are expecting a significant margin correction in FY 2023 (ICRA).

• India’s finished steel exports are expected to decrease by 25% y-o-y in FY 2023. However export of semis is likely to increase by 40% yoy in the current fiscal.

• Indian steel mills have announced large scale expansion plans, which would lead to capacity increasing by 40 million tonnes per annum (MTPA) during 2022-2026.

• Global steel market is projected to post a CAGR of 4.1% to reach 2.2 billion MT by 2026.

• With expected investments in infrastructure, domestic steel demand is expected to increase at a CAGR of 10% till 2026.

Chiana can decide the price of steel the Indian companies expansion plans and decrease in exports will be harmful effects in results Indian companies face very competitive prices and lost profits