Capital goods sector – Engineering the next phase of growth

India’s engineering exports have grown impressively over the years, but the sector needs to move beyond low- and medium-technology products.

The capital goods sector has been the clear outperformer in terms of engineering exports, but is still operating way below its potential.

The government announced the National Capital Goods Policy in 2016 to increase production capacities, ramp up employment and cut down on imports.

To achieve sustainable growth, capital goods players need to invest in building scale and innovation in futuristic technology domains.

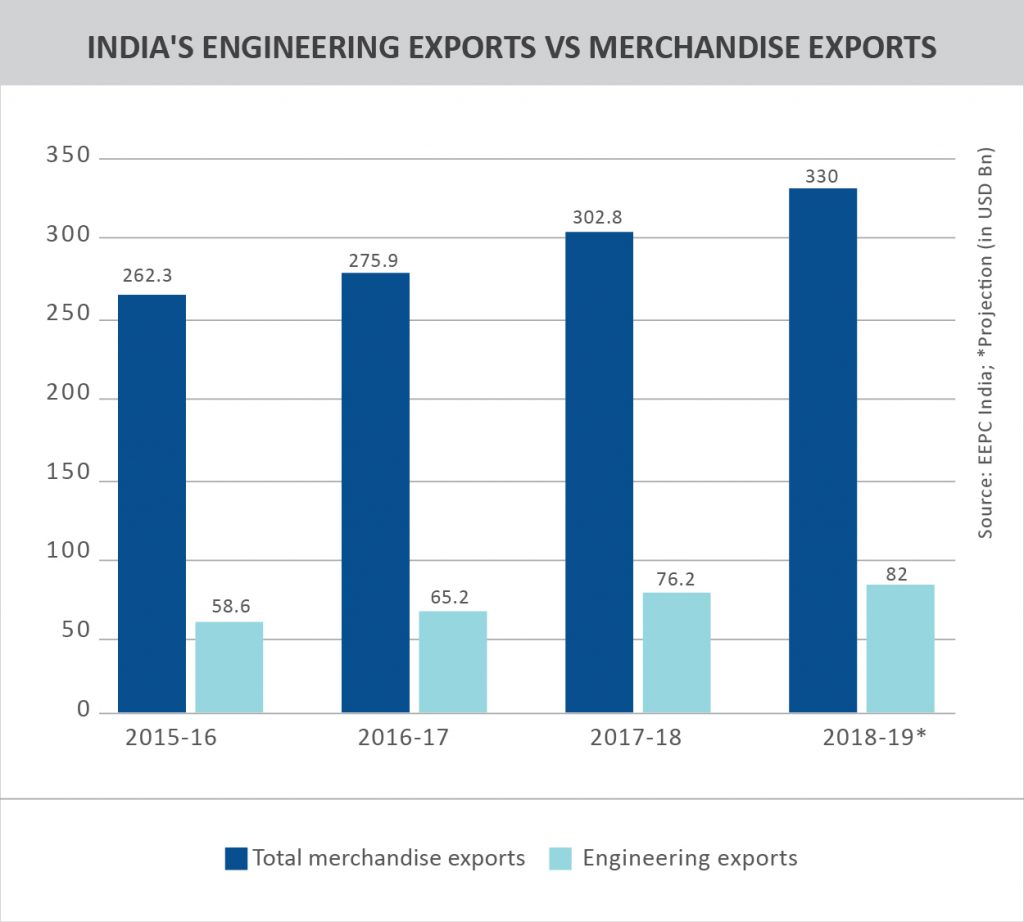

The engineering sector is the highest contributor to India’s export basket, accounting for around 25% of total exports by value. India has earmarked a target of US$ 200 billion for engineering exports by 2025. A roadmap to achieve this target has been suggested by an EEPC India-Deloitte strategy paper, with inputs from the Department of Commerce as well as members of the industry.

The paper was released at the recently concluded International Engineering Sourcing Show (IESS) Chennai, and identifies a conducive ecosystem, product-market optimisation, branding and competitive input prices (especially steel) as critical factors to achieve the target. External factors like global macroeconomic situation, investment made by the industry, performance by competitive nations and trade policies would also have a bearing on India’s progress towards achievement of this target.

Transformation in product-market mix

Engineering exports posted a growth of 16.81% yoy to reach a record US$ 76 billion in 2017-18. In the current fiscal, exports are expected to reach US$ 80-82 billion. Over the years, India’s engineering exports have diversified significantly vis-à-vis both products and markets.

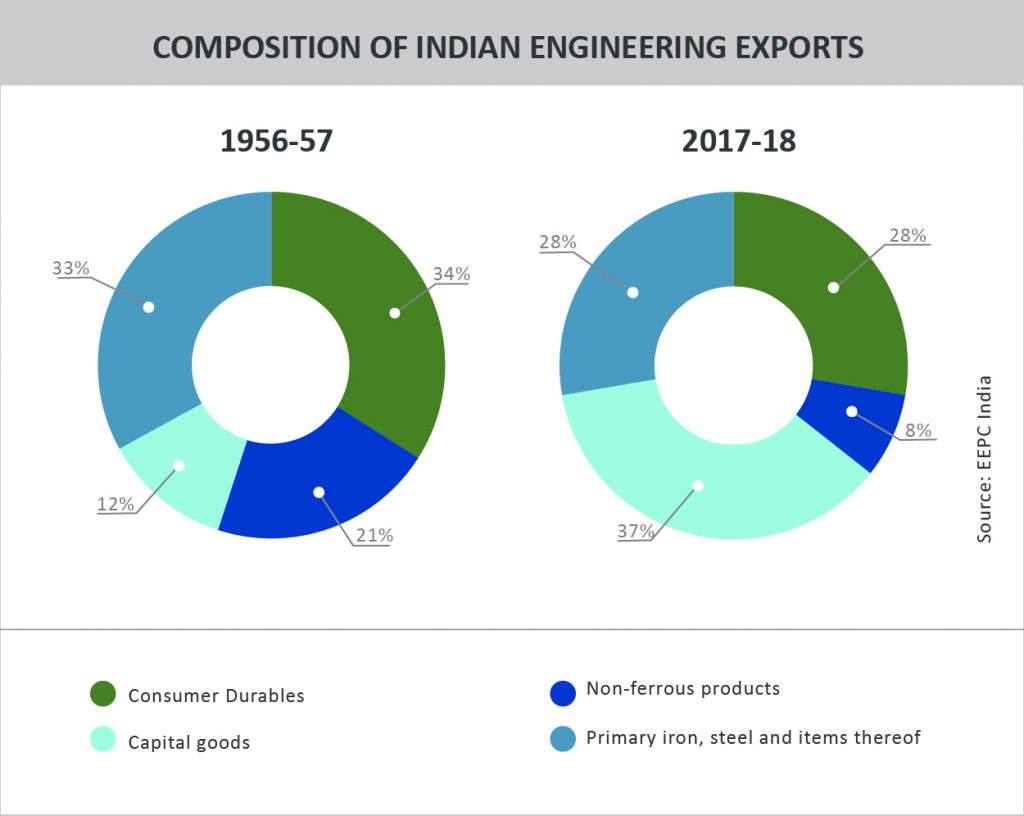

In terms of share of total engineering exports, the capital goods sector has clearly stood out, accounting for 37% share in 2017-18 compared to 12% in 1956-57. The share of primary iron & steel and items thereof has decreased from 33% to 28%, and the proportion of consumer durables has reduced from 34% to 28% during the period.

When we compare the share of export destinations, the change is even starker. In 1956-57, Asia was the destination for 74% of engineering exports and Africa had a share of 23%. But by 2017-18, the portfolio has considerably diversified, with EU (21%), North America (18%), ASEAN+2 (13%) and Middle East & West Asia (11%) as the leading export destinations.

While engineering export performance has improved significantly, the EEPC-Deloitte report asserts that India still hasn’t achieved leadership in any category, and still continues to export low- and medium-technology products.

A case in point is the capital goods industry itself, which forms the largest share of engineering exports, and provides around 1.4 million direct and 7 million indirect jobs. The sector accounts for 12% of total manufacturing in India, and its largest subsector is electrical equipment, followed by plant equipment and earth moving/mining machinery. Although this sector has been the highlight of India’s growing engineering prowess, it still has a long way to go.

Enhancing competitiveness of the capital goods sector

The Government of India announced the National Capital Goods Policy in 2016, which aims to increase production from Rs 230,000 crore in 2014-15 to Rs 750,000 crore in 2025, and raise direct and indirect employment to 30 million. Furthermore, the policy targets increasing exports from 27% to 40% of production and growing the share of domestic production in India’s demand from 60% to 80%.

However, the sector is still operating well below its potential at 0.6% of India’s GDP, compared to 4.1% for China, 3.4% for Germany and 2.8% for South Korea. Despite exports having grown significantly over the years, India isn’t able to meet its domestic demand for capital goods across sectors. During 2010-2015, the demand for capital goods increased at a CAGR of 10%, while the sector itself grew at a CAGR of 2%.

A report prepared by McKinsey for the FICCI Capital Goods Committee identifies a number of factors hampering growth of the sector. Indian players invest around 0.5% of their turnover in R&D. In comparison, companies in Germany invest around 6% of their turnover. Capital goods accounted for only around 4.4% of total FDI into India during 2000 to 2015. Other priority areas for the sector include attracting quality talent, building a high quality domestic supplier base and leveraging G2G (government-to-government) engagements with other countries.

While India has made great improvements in terms of Ease of Doing Business, there is still considerable work to be done to improve competitiveness. For instance, if India’s logistics costs are brought down from 14% to 9% of GDP, the consequent savings will amount to US$ 50 billion according to an Assocham report.

Futuristic growth opportunities

Moreover, capital goods players need to invest in emerging growth segments to drive sustainable growth. These include environmental solutions (like emission control equipment, output water treatment and recycle/reuse systems, etc); logistics infrastructure (railway, metro, ports, etc); aerospace & defence; urban infrastructure (water management, waste management, power, smart city solutions, etc); power (engineering, procurement & construction, components, grid upgradation, renewable energy integration, etc) and food infrastructure (fertilisers, farm mechanisation, etc).

Trends in the technology landscape and proliferation of digital technologies in manufacturing could be game changers for the sector in the coming years. The emergence of Industrial Revolution 4.0 is visible in the proliferation of Internet of Things, sensors, robotics, etc. With the help of technologies like 3D printing and automated real time processes, the cost of production can come down sharply.

India’s manufacturing competitiveness is improving at an impressive pace. A study by Deloitte predicts that India will jump six places to rank 5th in manufacturing competitiveness by 2020. India’s manufacturing labour cost was estimated at US$ 1.72/hour in 2015, half of China and way below US$ 37.96/hour for the US.

The Indian capital goods sector needs to leverage this growing competitiveness to build scale and invest in innovation, particularly in emerging technology areas. This will enable the sector to enhance its global presence, while also clamping down on rising imports.

Leave a comment