Aluminium industry: Dying a slow death?

• Rising imports of aluminium have been a source of major concern for the domestic industry over the past few years.

• Imports from China have been a major contributor to this rising trade deficit, exacerbated due to the high import duties imposed by it on scrap imports from the US.

• India’s trade deficit in aluminium is likely to worsen with China adding aluminium scrap to its ‘Restrictive Imports List’.

• A focused and strategic approach is necessary to both tackle the threat of dumping and improve India’s self-dependence in the aluminium sector.

Aluminium, a non-renewable resource is of immense strategic importance to India, one of the fastest growing economies in the world. A number of sectors including power, automobiles, construction, packaging, industrial and consumer durables are dependent on this metal.

However, a significant proportion of this precious metal is imported into India to meet the huge domestic consumption. And this is the scenario when aluminium consumption in India at 2.5 kg per capita is way below the global average of 11 kg per capita.

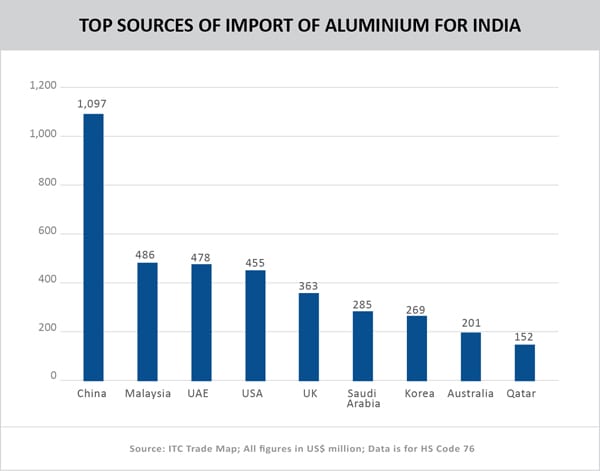

Over 55% of the aluminium demand is met through imports at present, with China as the largest contributor. Imports from China in particular have risen sharply over the past few years from US$ 642.7 million in 2014 to US$ 1.1 billion in 2018 (ITC Trade Map). Correspondingly, India’s exports of aluminium to China have been insignificant and in fact declined from US$ 13.29 million in 2014 to US$ 11.1 million in 2018. India’s northeastern neighbor provides several incentives to its aluminium industry like interest free and low cost loans, subsidised land on new smelter projects, income tax rebates and transport subsidies.

Slowly and steadily, China has succeeded in not just reigning supreme as the largest consumer, but also as the largest producer of aluminium in the world. Indian exporters have not been successful in tapping the huge potential that the Chinese market offers.

The China factor is also harming India’s interests indirectly on another front with its decision to add aluminium scrap to its ‘Restrictive Imports List’ from July 2019. Due to the trade war, China has also increased tariffs on aluminium scrap imports from US to 25%. As China builds barriers to scrap imports, India is emerging as a natural destination for dumping of the product.

Furthermore, low import duties on aluminium scrap (2.5%) have eroded market shares of the domestic aluminium industry. Players like Vedanta Ltd, Hindalco Industries & National Aluminium Company (Nalco) have borne the brunt of this development, as their market shares dropped progressively from 60% in FY’11 to 40% in FY’19.

A NITI Aayog paper identifies aluminium as a strategic sector for India going forward. It would greatly help enhance the fuel and cost efficiency of railways, India’s commitment to CO2 emission norms, adoption of electric vehicles improve the share of renewable energy to 40% and beyond and promote indigenization in defence equipment, aerospace and aviation sectors. But the sector faces a number of constraints at present.

High cost of production is a major issue, led by high power costs that account for 30-40% of production. Mining of bauxite and coal also faces challenges with delayed clearances, bad connectivity, land acquisition issues, etc.

Given the low competitiveness of the industry, it is not surprising that countries like China has been able to make deep inroads. As Professor Anwarul Hoda, Chairperson, ICRIER affirms in his conversation with TPCI, “With plentiful bauxite reserves, India is highly competitive in aluminium, but its competitiveness is affected by the mining policy and poor transport infrastructure in the country. As a result China has been able to price aluminium more competitively in world markets and export large quantities into India despite import tariffs”.

Given the current scenario of possible dumping of aluminium scrap, immediate increase of import duties on the product is a must. India has sufficient aluminium scrap, and imports need to be restricted to boost domestic recycling. The industry has also alleged that China is breaching Rules of Origin and routing aluminium exports to India through ASEAN nations, for which the government should immediately consider appropriate safeguards.

But that is only a short term fix. India needs to cut down its import dependency for aluminium, given that its strategic relevance is only expected to surge with rising economic growth. To ensure that, India must draft and implement a National Policy on Aluminium with specific short, medium and long-term targets for both demand augmentation and capacity addition, along with the necessary policy impetus to achieve them.

Leave a comment