Decoding India’s Plastic Import Surge: A Path to Self-Sufficiency

India’s increasing reliance on plastic imports with a sharp rise this year urged CATR to decipher this dependence and look for ways to balance the situation. With the right policies in place, the industry has the potential to decrease the negative trade balance and increase its global footprint.

- India imported US$ 19.15 billion in plastics in 2022-23 (Apr-Jan) whereas exports registered a negative 13.84% YoY growth during the same period.

- The country is seen relying on imports majorly for cheap raw materials along with some huge structural challenges in downstream products manufacturing.

- The industry needs cheap raw material availability, supportive infrastructure, and opportunities for export expansion. Investments in recycling and reusing can act as the most sustainable ways.

- According to our research analysis, products like plates, foils, films (HS 3920) and other plastic products (HS 3926), have domestic production capacity to cater to the demand, and with policy support can reduce import dependence.

Image: Shutterstock

Plastics have been playing a predominant role in shaping our lives. 100 years young in comparison to traditional materials, plastic has accounted for a global production of 367 MT in 2021. Being the third largest consumer of plastics, India’s share of global plastic use is 6.4% and stats reveal a projection of 160.4 million tons use in India by 2060 from an estimated demand of 15 million tons in 2021-22.

The Indian plastic industry has made significant achievements since its inception with the production of polystyrene in 1957. By catering to an entire spectrum of daily use items of life since ages, per capita consumption of plastics in India is estimated at 15 kg in 2021, from 13.6 kg in 2018.

Value chain of plastics

The plastic industry in India is closely intertwined with the petrochemical industry. It starts with the raw materials, such as natural gas, oil or plants and is refined into ethane and propane. These compounds on heating are thus converted into monomers which on combining with catalysts become polymers. These polymers are then converted into plastics.

The industry comprises both upstream and downstream activities (conversion of polymers). The downstream manufacturers cater to multiple industries across the country with industries like, automotive, construction, electronics, healthcare, textiles, and FMCG.

To cater to the needs of different sectors, a wide variety of plastic raw materials are produced. Commodity plastics (the bulk of the plastics produced) include Polypropylene (PP), Polyethylene (PE) and Polyvinyl chloride (PVC). The rests are Engineering plastics and Specialty plastics, produced for special purposes with a wide variety of properties.

India’s overall production infrastructure for petrochemicals is mainly driven by a limited number of oil refineries and standalone petrochemical companies.

According to the polymer landscape study, West India accounts for the maximum share (61%) of upstream plastic manufacturing, followed by Northern India with an 18% share, East India accounting for 15% and Southern India having the least capacity with only 6% share.

Whereas, the downstream plastic processing sector in India is primarily dominated by Indian companies. Small/medium-scale enterprises hold nearly 85% of the industry.

Where on the one hand, India’s MSME exports downstream products, and the upstream polymer industry is highly import dependent. With a target to export US$ 25 billion for FY 2024-25, India’s exports of plastics registered a negative 13.84% YoY growth in 2022-23 (Apr-Jan) with an estimated value of US$ 6.49 billion. On the other hand, imports touched US$ 19.15 billion over the same period. Industry’s increasing dependence on imports has brought apprehension but with the right policies in place, the industry can decipher a way to expand its global footprint.

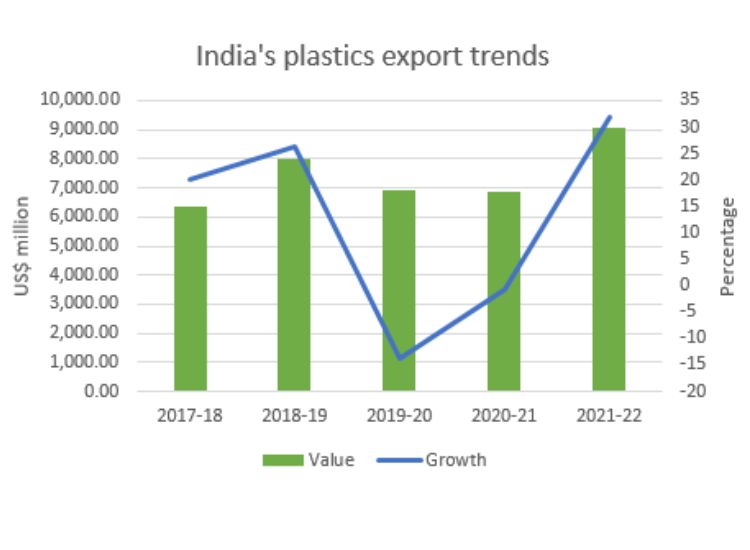

After registering a 31.74% YoY growth in 2021-22, India’s plastics exports are expected to almost double for the period 2024-25. Despite supply chain disruptions during Covid-related lockdowns, exports not only recovered but witnessed emphatic growth. Being ambitious about these growth trends, The Commerce and Industry Minister, Mr. Piyush Goyal sets a target for the domestic plastics industry to grow its size to Rs 10 lakh crore in the next 4-5 years from Rs 3 lakh crore in 2022 while speaking at Export Excellence Awards by Plastics Export Promotion Council (Plexoconcil).

Source: Ministry of Commerce and Industry

The country’s plastics exports have registered a 9% CAGR over a period of 4 years, with a total value of 9.05 billion in 2021-22. Following are the top 75% exports of plastics out of which (3920) Other plates, sheets, films.., (3907) Polyacetals, (3923) Packaging articles… (3926) Articles of upstream products (3901-3914) and (3921) other plates and sheets..were the major exported products registering positive YoY growth.

| HS code | Commodity | Value of exports in 2021-2022

(US$ million) |

YoY growth (%) | Share in total exports of 39 (%) |

| 39 | Plastic and articles thereof. | 9,052.37 | 31.74 | |

| 3920 | Other plates, sheets, film, foil … | 1,438.00 | 33.35 | 15.9% |

| 3907 | Polyacetals | 1,405.22 | 59.91 | 15.5% |

| 3923 | Articles for the packaging goods | 1,127.87 | 29.58 | 12.5% |

| 3926 | Other articles of plastics of headings 3901 to 3914 | 895.45 | 45.51 | 9.9% |

| 3901 | Polymers of ethylene in primary forms | 766.73 | -9.52 | 8.5% |

| 3902 | Polymers of propylene.. | 745.85 | -2.36 | 8.2% |

| 3921 | Other plates, sheets, film, foil and strip, of plastics | 405.04 | 22.93 | 4.5% |

Source: Ministry of Commerce and Industry

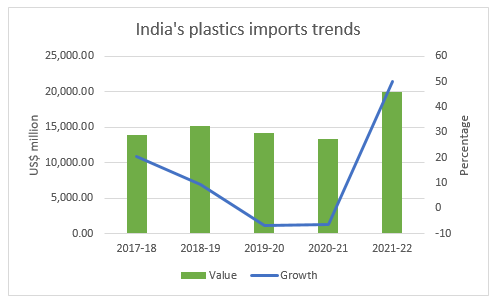

With the kind of growth trajectory that India is on, accessing the nation’s increased dependence on imports becomes vital. Plastic imports have grown more than what has been exported. The country imported US$ 19.99 billion in 2021-22, establishing 50.24% YoY growth.

Source: Ministry of Commerce and Industry

All the products in the top 75% of imports of plastics have registered a positive YoY growth showing increasing reliance on imports in 2021-22. (3901) Polymers of ethylene, (3904) PVC, Polyacetals, (3920) Other plastics from polymers were some of the highest imported products.

| HS code | Commodity | Value of imports in 2021-2022

(US$ million) |

YoY growth (%) | Share in total imports of 39 (%) |

| 39 | PLASTIC AND ARTICLES THEREOF. | 19,994.19 | 50.24 | |

| 3901 | Polymers of ethylene in primary forms | 3,235.65 | 46.93 | 16% |

| 3904 | Polymers of vinyl chloride (PVC).. | 3,116.47 | 57.84 | 16% |

| 3907 | Polyacetals.. | 2,490.60 | 57.29 | 12% |

| 3902 | Polymers of propylene.. | 1,765.59 | 70.63 | 9% |

| 3920 | Other plates, sheets, film, foil.. | 1,668.06 | 56.27 | 8% |

| 3926 | Other articles of plastics (3901 to 3914) | 1,198.95 | 26.21 | 6% |

| 3909 | Amino-resins, phenolic resins.. | 809.25 | 46.24 | 4% |

| 3908 | Polyamides in primary forms | 732.43 | 78.4 | 4% |

Source: Ministry of Commerce and Industry

After running an analysis on the top 75% of imported products, we could map out 2 downstream products which have domestic capacity and with the right set of policies in place, India can reduce their import dependence. Plates, sheets, films, foil and strips.. (HS 3920) and Articles on plastics.. (HS 3926) are these two shortlisted products.

Rightly skewed imports

Indian plastic value chain, classified into Upstream and Downstream plastics, faces severe challenges in upstream production. The demand for polymers (raw material) is satisfied with increased imports and major raw material production has remained concentrated with few big manufacturers. The industry’s high dependence on imports is majorly concentrated in low-cost raw materials. The main challenge for them is the availability of polymers at competitive prices in India.

Indian plastic exports, dominated by exports from MSMEs (65% share), face many structural challenges. Indian processors are not at a level playing field when compared to the cost of production enjoyed by the competitors in the ASEAN region. High input costs of raw materials and levied cross-subsidy on power supplied to industry to give subsidized power to farmers raise production costs. Irregular power supplies were also found to raise the costs of production. Lack of access to ports is an even bigger issue for exporters. Places near ports are expensive and are difficult to set up large capacity units. The procedure of securing permission to set up and operate plastics manufacturing plants is another bone of contention and differs from state to state.

Need of the hour

On the journey to becoming ‘aatmanirbhar’ (self-reliant), India has to consider ways to reduce its import dependence on its plastics. With a significant growth potential, various sectors like packaging, agriculture, electronics, housewares, transportation, furniture, etc. are high consumers of plastics. Few structural changes have the capacity to clear the bottlenecks for Indian manufacturers which can be broadly divided into categories.

Lower the cost of feedstock: The industry’s main challenge and the biggest impediment is the availability of raw materials at lower costs. In the short term, reducing tariffs on imported raw materials until Indian manufacturers build capacity to cater to domestic demand will bring significant changes. Raw materials attracting higher duties than their final products spoil the industry dynamics and domestic manufacturing units face back-breaking competition for input costs.

Build Infrastructure: To build scale for the long term, better infrastructure is required which will bring a decrease in manufacturing and logistics costs. The government’s initiative of having Petroleum, Chemical and Petrochemical Investment Regions (PCPIR), is a step in this direction. They would have a high-class infrastructure, and provide a competitive environment conducive to setting up businesses. They would thus result in a boost to manufacturing, augmentation of exports, and generation of employment.

Globalize with localize: Negative trade balance can be reduced by increasing exports. India’s aim to have upward-sloping exports can be supported by having mutually beneficial Free Trade Agreements. Despite India’s major plastic exports to markets like the US (16.3%) and WANA region (14%), there are no FTAs with the countries, due to which the exporters are unable to realize their full potential.

Incentivize manufacturing and exports: The inclusion of Petrochemicals in the production-linked incentive (PLI) scheme will give a boost to domestic manufacturing, investments, and exports in the sector. Measures to improve ease of doing business along with improving clearance assessment systems will also work in the same direction. Smooth application of schemes like Merchandise Exports from India (MEIS), which is to give benefits to the exporters will boost exports. Schemes like these to offset infrastructural inefficiencies and associated costs involved in the exports of goods.

Recycle the used: Plastic industry can resort to recycling and reusing used plastic in order to reduce its reliance on virgin raw materials. In the words of Dr. R Vasudevan, also known as the Plastic Man of India,

The country should adopt ‘indovations’, i.e India’s way of innovatively reusing it’s plastics and reducing foreign dependence. The country with all the present technology and also by investing on R&D, can find out ways to generate plastics. Plastics, which can not be recycled due to complexity, should be reused. For example, it is nearly impossible to recycle a chocolate wrapper made up of three layers, aluminum, polythene and polyester. But by adopting innovation the industry can easily reuse it.

This will not only reduce investments in procuring raw materials but also be a green solution.

Conclusion

The plastic industry is assured to grow at a good rate with a major focus on factors like per capita consumption, manufacturing capacities, end-use industry, and availability of feedstock. Low costs inputs and better infrastructural facilities are the fuel for the industry’s growth. Resorting to recycling and reusing can be the two most sustainable tools in today’s scenario. Government and industry both should not hesitate in joining hands in making the country a global manufacturing hub.

Leave a comment