India’s FAB challenge: Need for a new business model?

Dr Sunitha Raju, Professor at Indian Institute of Foreign Trade, feels that considering the high investment for developing the semiconductor manufacturing ecosystem, fabless companies are a viable option for India with its design capabilities. But this depends on how India is able to integrate with the OEMs, such that the demand for these chips can be sustained.

The current global shortage of chips raises questions on the dynamics of supply and demand of the global semiconductor industry. The IDC forecasts the semiconductor market to reach US$ 522 billion in 2021, a 12.5% growth over 2020. The worldwide semiconductor sales increased from US$ 14 billion in January 2009 to US$ 42 billion in January 2021 (SIA, June 2021). This acceleration in demand is largely due to technological advances and development of industry devices for AI, IoT, 5G, AR/VR. Through the integration of these with end user industries like automotive, networking, robotics, mobile, PCs, the demand for chips has increased along with high efficiency and computing power.

On the supply side, two important dimensions stand out. One, as the manufacturing of chips is running at full capacity, capacity expansion is underway.

Twenty nine new fabs/foundries are being set up in different locations by 2022 with an anticipated production capacity of 2.6 million wafers per month. Of the 29 fabs, China and Taiwan account for 8 fabs each, US 6, Europe 3, Japan & South Korea 2 each.

Two, the supply chain of semiconductor industry is highly specialized and globally integrated across many countries. The US leads in R&D intensive activities like electronic design automation, core intellectual property, chip design and advanced manufacturing equipment and East Asia dominates wafer fabrication which requires capital investment and skilled workforce. And, China dominates the assembly, packaging and testing. All countries are interdependent with each country specializing in their different roles according to their comparative advantage.

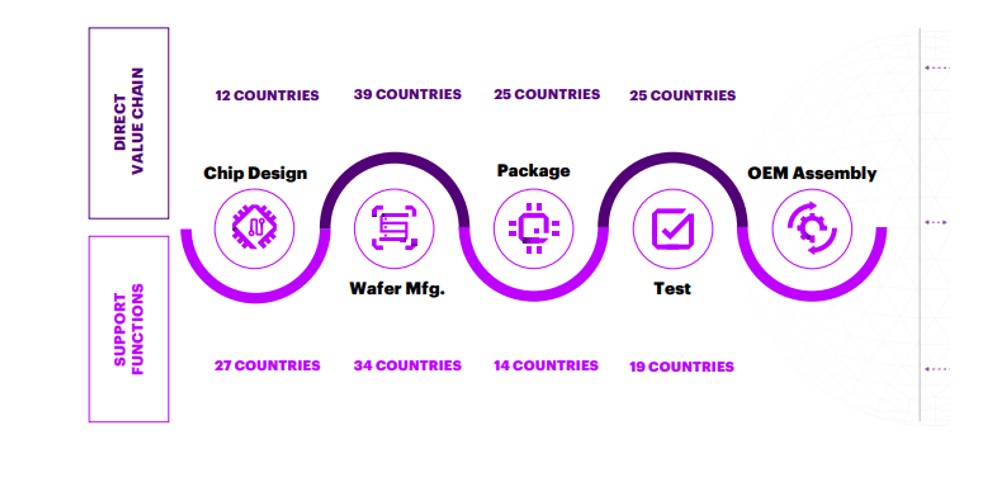

As such, this global value chain is critically dependent on free trade to move materials, equipment, IP, products across these different locations. This global collaboration which determines the success of the semiconductor industry can be gouged by the countries involved at each node of the supply chain as given in Figure 1.

Figure 1: Semiconductor manufacturing value chain and countries engaged

Source: Accenture GSA (2019), “Globality And Complexity of the Semiconductor Ecosystem”

Given the criticality of each country’s specialization in every node of the supply chain, any disruption in one node can cause complete halt to the production of the end user industries. The natural disasters in Taiwan and Japan resulted in shortage of chips, the US-China trade war and disputes between Japan and S Korea have caused serious disruption to this integrated global supply chain of semiconductors. As such, particularly with the ongoing Covid pandemic, many countries have voiced out about developing complete value chains nationally. Considering the enormous scale necessary to justify the huge capital investment, developing a national value chain can entail an incremental investment of US$ 1 trillion and an overall increase in semiconductor prices by 35% to 65% (BCG & SIA, 2021).

India has also voiced out the need for developing a national value chain for semiconductors, mainly to address the surge in imports of electronic goods and components and to reduce the dependence on China. The National Electronics Policy (2012, 2019), PLI, EMC, SPECS are all efforts towards this end. The question is: without being a part of the global value chain, can India succeed in these efforts? In the broader context of ‘Go Local’ and ‘Atma Nirbhar’ what does developing semi conductor value chain mean? And, what are the necessary conditions for India to develop this value chain (wholly or partially)?

Semiconductor Supply Chain: A Snap Shot

Semiconductors are integrated circuits, commonly referred to as chips. These chips are miniaturized electronic circuits composed of many electronic components and the interconnections between them are layered on thin wafers of semiconductor material. The smaller the chip size (measured in nm, nano meter), the higher is the computing power. In 1987, the chip size was 800nm, in 2020 it is 5nm and by 2023 it is expected to be 2nm. As such, chip design is highly R&D intensive.

The semiconductor industry is the aggregate of companies engaged in design, fabrication of semiconductors (foundries) and semiconductors devices (ICs). While the industry taxonomy of products categories are more than 30, semiconductors are classified into 3 broad categories.

First, the Logic ICs, account for 42% of industry revenue and covers microprocessors, General purpose Logic, Microcontrollers and Connectivity products. Second, Memory Products account for 26% of industry revenue and covers products like DRAM (Dynamic Random Access Memory) and NAND. And third, DAO (Discrete, Analogue and Others) account for 32% of industry revenue.

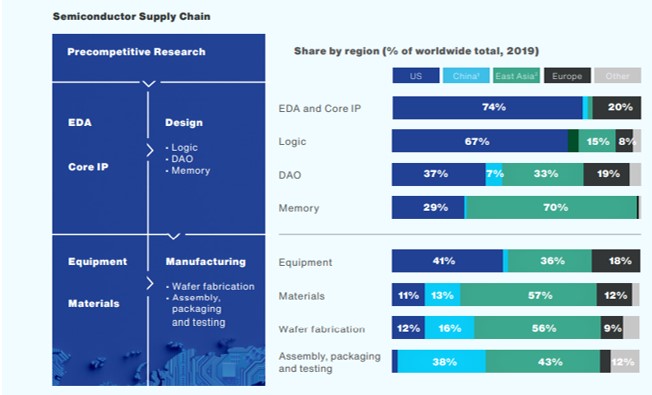

The structure of the semiconductor supply chain and their geographical specialization is detailed in Figure 2.

Figure 2: Global Semiconductor Supply Chain and Geographical Specialisation

Source: BCG & SIA (2021), “Strengthening The Global Semiconductor Supply Chain In An Uncertain Era”.

In the pre-competitive research, US dominates in the design of Logic and core IP while East Asia (Taiwan, Japan, S Korea) dominate in Equipment, materials and wafer fabrication and China in Assembling and testing.

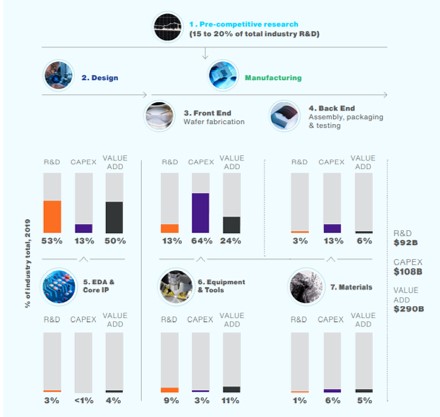

The differentiated activities in the supply chain in terms of their intensity in R&D, Capex and Value added are given in Figure 3. The significant activities are design and manufacturing (front end). While design accounts for 53% of industry R&D and 50% of value addition, Wafer fabrication accounts for 64% of Capex and 24% of value addition. Despite these activities contribution, all other activities are necessary for completing the value chain and therefore are indispensable.

Figure 3: Semiconductor Value Chain: R&D, Capex And Value-Added

Source: BCG & SIA (2021), “Strengthening The Global Semiconductor Supply Chain In An Uncertain Era”.

Semiconductor Industry: Where Does India Stand?

The demand for semiconductors in India is increasing exponentially. As per the estimates of IESA (India Electronics and Semiconductor Association), India’s consumption of chips was placed at US$ 21 billion in 2019 and is expected to grow at 15.1% annually. Along with the objective of catering to the domestic demand and capitalizing on the growing global demand, the policy frame has been to manufacture chips in India.

The policy push has been to strengthen design and manufacturing under the framework of ESDM (Electronic System Design and Manufacturing). As per DeitY estimates, India’s design market is projected to grow from US$ 14.5 billion in 2015 to US$ 52.6 billion in 2020 at a projected CAGR of 29.4%. DeitY has also asserted that India has a strong design base with more than 120 units and 2,000 chips are being designed every year.

While India does have design capabilities such as networking, microprocessors, analogue chip design and memory subsystems, all these are in the R&D divisions of the multinationals (Texas Instruments, NXP, MediaTek, AMD) that have subsidiaries in India. As such, India does not have a proprietary right on the design outcomes. Some of the start ups with chip design services have been acquired by these multinationals. A case in point here is the acquisition of SmartPlay by Aricent for Rs 1,100 crores.

Over the years, India has gained some competence in PCBA (Printed Circuit Board Assembly), largely used in mobile phones. As pointed out by ICEA, India can cater about 90% of PCBA market estimated at US$ 16 billion in 2020 and expected to reach US$ 87 billion by 2025-26.

The government’s efforts to bring in investments into design and manufacturing have not been very encouraging. Way back in 2007, government’s delay in semiconductor policy made Intel shift its plant to Vietnam. Also, the government’s initiative for international cooperation for setting up a fab unit in India, Hindustan Semiconductor Manufacturing Corporation, was cancelled in 2019.

In recent years, the government initiated many policies for establishing FAB units and supporting infrastructure in India. Some of these are EDF (Electronic Development Fund), EMC (Electronic Manufacturing Clusters), ESDM, SPECS , M-SIP, PLI. Despite these incentives, investments for setting up fab units from global majors like TSMC, Intel, Samsung have not been forthcoming.

Against this background, a quick review of the status of the semiconductor industry in India will provide the significance of these policy measures and point to workable models that can be looked into.

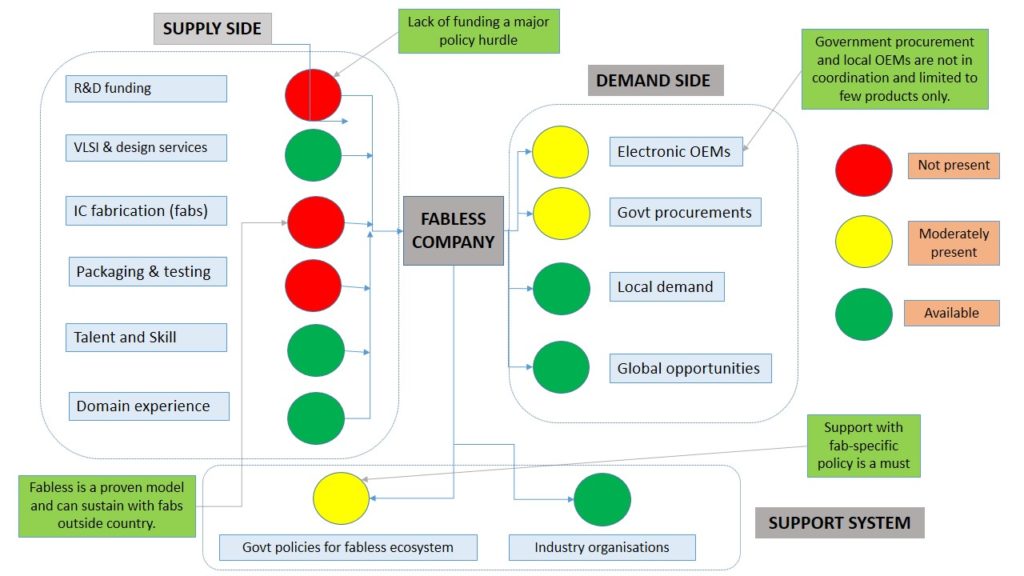

Figure 4: Status of Semiconductor Industry in India

Source: IESA (2018), “Indian Semiconductor Fabless Start Up Ecosystem: Opportunity Analysis and Strategic Plan”

From India’s point of view, the supply side constraints are R&D funding, Fabrication unit and OSAT. Chip design and manufacturing are highly capital intensive (see Figure 3). A fabrication facility for chip manufacturing requires an investment of US$ 8-10 billion and recurring investments as technology evolves. Unless the commercial viability of such investment is evident, private investors will not be forthcoming. Commercial viability is determined by scale and efficiency, which would mean catering to domestic market is not adequate. For production to take place in India, the market orientation needs to be global, which would mean engaging in trade with rest of the world.

Additionally, the cost and volumes depend on the manufacturing ecosystem. Chip manufacturing, being technology and capital intensive, necessitates the availability of specialized equipment. Approximately, over 50 equipments are required along the semiconductor supply chain. Some of them are Lithography tools, Metrology and inspection equipment and subsystems like optical or vacuum subsystems, gas and fluid management, thermal management or wafer handling.

In the absence of these critical precision equipment, efficiency and viability of the project will be uncertain. Therefore, the development of secondary industries around Fab units and companies that can provide critical services would constitute the manufacturing ecosystem. How far the current policy frame visualizes this complete ecosystem and envisages strategic options for taking action is not clear.

Considering the high investment for developing the manufacturing ecosystem, chip designers, more often, outsource to third -party manufacturers, what is called fabless company. This is a viable option for India with its design capabilities. This, once again, depends on how we are able to integrate with the OEMs, such that the demand for these chips can be sustained. In other words, the demand side issues for end-user industries need to be addressed and developed in order to bring in the volumes that are so necessary for the commercial viability of the semiconductor industry.

In conclusion, what this boils down is that domestic self reliance can only be realized with high trade engagement both for components as well as finished products. Servicing domestic market is not possible without looking at the global market. The semiconductor industry amply brings out this reality.

Dr. Sunitha Raju is a Professor at IIFT. She has 30 years of extensive experience in Education, Research, Policy formulation and Evaluation and held the positions of Chairperson (ICCD), Chairperson (Research) and Chairperson (GSD). Her areas of expertise include Trade Policy Formulation & Evaluation, Trade modelling, Agricultural Policy Analysis, WTO rules & Regulatory framework, Free Trade Agreements, Survey Research, Performance Reviews, Training & Management Development Programmes.

Great Insights ! We certainly need to take on the development and manufacturing of semi conductors on a war footing despite the constraints in supply chains.