India’s 5G playbook: Look before you leap?

Given the evolutionary nature of 5G networks, India needs to ensure rapid rollout of the technology to avoid being caught on the wrong end of the digital divide. But is India truly ready?

Sanjeev Nikore, Former President, Strategic Initiatives at Tech Mahindra & CEO, Strategies2Scale and Mitali Nikore, Founder Nikore Associates, discuss major infrastructure and financing constraints hindering 5G rollout in India, and propose critical regulatory interventions to address them.

Digitalization has pervaded just about every aspect of our life ever since COVID-19 struck the global economy early this year. It would have been quite unimaginable for segments like healthcare, government services, banks, education and supply chains to function without the interventions of digital technology. As physical interface became severely limited, the pandemic led to accelerated adoption of digital ways of living and working, be it through remote working, video conferencing, e-learning, e-commerce, OTT platforms or online gaming.

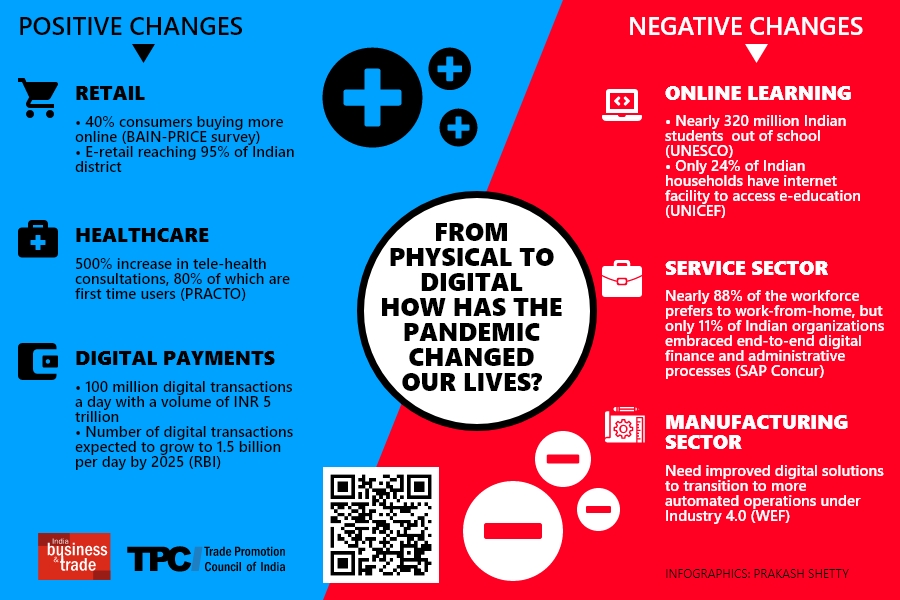

However, the post-pandemic situation has also brought the digital divide into sharp focus. (Figure 1). On one hand, sectors like retail, healthcare and digital payments have seen exponential growth. A BAIN-PRICE survey reveals that around 40% consumers are buying more online. We don’t know the worth of this basket, but it is still a massive increase. Around 95% of Indian districts are touched by an e-retail footprint, which makes it a game-changing market opportunity. Tele-health consultations have increased by around 500% according to Practo. The number of digital transactions are expected to increase to around 1.5 billion per day by 2025, compared to 100 million per day presently.

But on the flip side, the pandemic forced around 320 million students out of school, according to UNESCO. Correspondingly, UNICEF estimates that only around 24% of Indian households have the requisite internet facility to access e-education. Furthermore, only 11% of Indian organizations have end-to-end digital finance and administrative processes. Even India’s manufacturing sector currently lacks the best-in-class digital solutions needed to progress to Industry 4.0.

In this milieu, the entire debate on the adoption of 5G technology gathers an entirely new dimension. There is a general consensus that paradigms like remote working, video conferencing and OTT are here to stay, leading to an ever increasing demand for data.

Currently, there are close to 3.5 billion mobile connections globally. One hour of a live webinar requires 30-100 MB data transfer; standard definition (SD) quality video conferencing needs around 700 MB data transfer, while full HD requires even more. A US citizen uses an average of 5 GB data per month, while India is even higher at an average of over 11 GB.

Moreover, as we move towards technologies like AI, automation and IoT, 5G is no longer merely about a better, faster and more convenient way to be online. It is about digital equity. Countries that delay making the quantum leap to the next generation of communication technology risk getting caught on the wrong end of the digital divide.

A gap wider than several gigabytes

Currently, India’s digital economy is valued at US$ 200 billion, but India has a roadmap to take it to US$ 1 trillion. 5G is a revolutionary technology, which can give high bandwidth and speeds of up to 10 GB per second, which are not possible on existing networks. A lot of new applications can be created, like IoT applications for remote management/operations. Video quality gets ramped up, so you can access ultra HD video. Segments like virtual reality, telemedicine, tele-health, Industry 4.0, Edtech and digital healthcare will get a tremendous boost and many new applications will come through 5G.

From the export perspective, we have a lot of technology/IT services companies in India. They face bandwidth constraints when they are servicing for production support or application development, which can be addressed through 5G technology. Through network splicing in 5G, you can create dedicated networks for dedicated functions, like specific traffic management, transport management, warehousing, supply chain, etc.

5G will also be very helpful for MSMEs because of the creation of distributed cloud. This implies that they can access computing power, storage and networking on tap, much like electricity. You can use as much as you want, depending on what need and what you can actually pay.

Unsurprisingly, the world is expected to witness a proliferation of 5G technology in the coming years. The MIMO technology – multiple radio signals in and out – which is the basis of 4G, LTE & 5G – has now been adopted by many telecom companies. According to GSMA projections, 5G is expected to cover one-third of the world’s population by 2025. By around May this year, 5G connections had been deployed in 378 cities across 34 countries. Out of the 681 4G-based LTE networks worldwide, one-fifth are conducting field trials and testing 5G. AT&T, Sprint and Verizon have launched services in the US and China Mobile is going live this year.

Source: Nikore Associates

Steady the ship

In India, we have still not announced the auctioning for 5G spectrum, though the government has formed a Spectrum Management Framework for allocation of new spectrum. However, there are serious issues that India needs to tackle before it plans to roll out the technology, in order to ensure success.

Infrastructure gap: India has to ramp up its broadband and backhaul optical fibre network for the high speeds that 5G offers. The country has 1.5 million km on fibre, which it is expecting to increase to 2.5 million km by 2022. In terms of fibre km length per capita, however, India is considerably lower than Japan, China, Western Europe, etc. It is also one of the lowest amongst the BRICS. Mobile download and broadband speeds in India are presently around 55-66% lower than the global average. In the Global Connectivity Index, India ranks 65 out of 79 countries.

Capital investment: Our research shows that compared to the benefits of digital infrastructure, government investment is very low – at just around 0.2% of GDP. In addition, just around 20% of that is allocated to capital expenditure like setting up towers, laying down fibre cables, etc. Upgrading this infrastructure requires a lot of efforts and investments from the public and private sectors.

The Asian Infrastructure Investment Bank estimates India’s annual investment on digital infrastructure to be ~$20-22 billion, or 0.7% of GDP (2018). Despite this, pre-COVID-19 estimates from the Global Infrastructure Outlook show that India’s telecom sector faces a ~US$ 167 billion investment gap between 2015-2040. Interestingly, the picture is not exactly rosy for China either. They also have a large telecom infrastructure funding gap of around US$ 150 billion, and are investing less of their GDP in digital infrastructure.

But the major difference is that China is much faster at rollout, due to its technology and institutional capacity. In addition, some other Asian countries face lower financing gaps and are spending more on digital infrastructure. Since our gap as well as population are higher, India needs to invest more.

High costs of rollout: Around 70% of telecom financing in Asia is private sector-led, even as the government plays a key role. The Indian government has launched various initiatives over the years. BharatNet was aimed at providing high speed digital connectivity to gram panchayats. Digital India was launched to make a major shift to e-governance. As per the National Digital Communication Policy, an action plan for rollout of 5G had to be established, but COVID has led to hurdles in roll out of optical fibres, telecom towers, etc. Moreover, construction costs and right-of-way fees in India are among the world’s highest.

India also has among the highest reserve prices of spectrum, though a rethink is happening on licence fees. Spectrum cost is at around US$ 70 million in India vs US$ 18 million in South Korea, US$ 10 million in UK and US$ 5 million in Australia.

Private sector pains: India is unprepared for 5G rollout due to lack of profitability and cashflows. TRAI estimates that around US$ 60-70 billion in investment is required over the next 3 years to achieve a commercially viable 5G rollout. This requirement creates a huge infrastructure financing gap. Cumulative debt of the sector stands at around US$ 100 billion. Players are facing falling profitability, which constrains their investment capacity. Then there is the fibre connection deficiency – reaching 80% of telecom sites (currently 25% are connected through fibre) will require around US$ 8 billion in investments, according to Deloitte.

Among the private sector players, Reliance is in the best situation. They announced in their last AGM that they are almost 5G ready. But at the same time, we cannot have a monopoly. Other players need to upgrade their LTE infrastructure and get new 5G radios. They will require major upgrades to their network infrastructure as 5G networks will be fully virtualized and cloud native.

Source: Nikore Associates

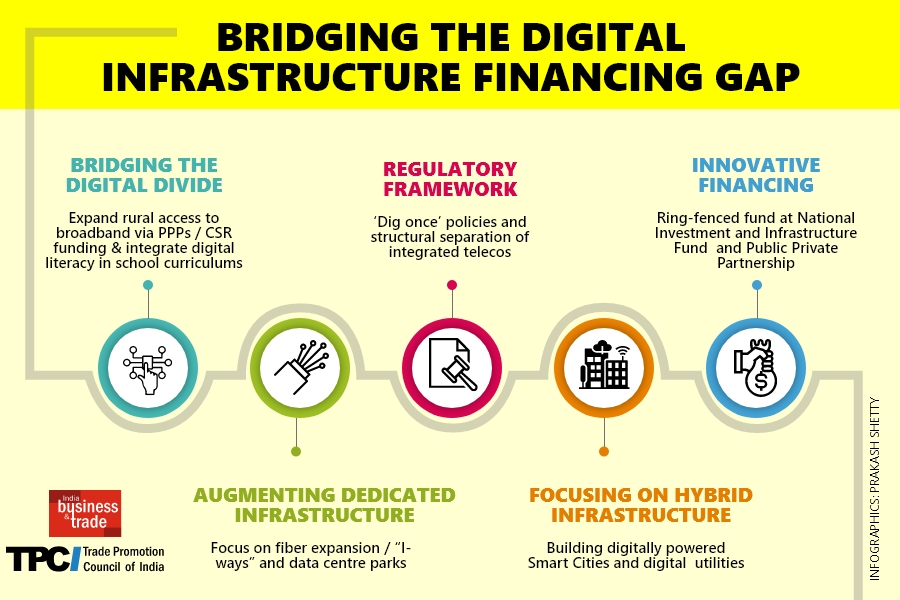

Dig once, improvise for many

It will be very important for the government to have a level playing policy framework, and also ensure certain facilitators from a financing perspective for healthy competition. Other players like Google and Microsoft could also come in, because a lot of cloud element native development is required for 5G to be effective. Google, Facebook and Microsoft have partnered/invested in Reliance JIO, and other players are gearing up. So there could be interesting tie-ups.

Telecom players should be able to benefit from cross-subsidisation across the market. At one end, high-income earning customers are willing to pay for premium services. On the other end, there is a huge market segment that can only afford basic connectivity. So you need to have differentiated pricing, which is not the case right now, due to lack of competition.

TRAI needs to lobby with Invest India and DIPP to bring more players into India by introducing a predictable tariff regime. The minimum tariffs and levels of service have to be specified. Private players need to be given freedom to offer premium services and innovate on their service bundles to provide more value. If the pricing landscape does not change, we will not see an improvement in quality. This kind of regime has been successfully introduced by countries like the UK.

Then there is the ‘dig once’ policy adopted by Singapore, Japan and some countries in Europe. You don’t keep digging your infrastructure again and again to lay cables, water lines, fibres etc, and then construct roads. In India, however, the problem is that different public departments do not communicate effectively with each other. Consequently, the cost of construction will keep on ballooning. Dig-once policy should also be enforced by the Central Government in India through a top down approach.

Structural separation of telecom companies is done very effectively in Singapore, Australia and UK. The person supplying the fibre connection is different from the company giving you the final mobile connection. So the company is delivering fibre at the national level to consumer facing companies. That helps end the monopoly situation.

These countries deploy a distributed architecture where the local or regional loop is being served by different distribution companies, who are into giving specialized services to clients. So you don’t just depend on the long haul; you allow the short haul to innovate, be more customer facing and create a superior customer experience.

Ringfenced funds and multilateral development banks

As indicated, companies are not in the best position to invest, especially when profitability is worsening. For 100 Mhz, they have to incur a minimum investment of Rs 49,000 crore. This builds a strong case for innovative financing models. Fortunately, funds are structured for this. For instance, India has a National Investment Infrastructure Fund in place. We could not find a specific head catering to digital infrastructure under this, although they work on technical, trade and social projects. More proper structured delineation for digital infrastructure would be a welcome step.

The idea of PPPs is that on one side, the government foots the bill for initial capital investment. This allows innovative private players to come in to design, build and operate, and then transfer it back to government ownership. Countries like New Zealand have successfully used PPP to fund their fiber rollout.

We need a clear ring-fenced fund – if a private player is coming in and enter into a PPP, they need to be secured that regular payments will be made. Having a ring-fenced fund under NIIF would bring credibility to such an initiative. That is how we can use private capabilities, expertise, private finance and public investment support required to hasten 5G rollout. Having PPPs helps bridge the digital divide. We have to cater to tier 2, 3 towns and rural areas also not just Delhi and Mumbai.

Considering the constraints we face, there is no need to obsess with having 5G in rural areas immediately, when they do not have broadband. There are other ways like satellite communication. ITC set up e-choupals as early as 2002-03, where they used VSATs for electronic trading with the mandis for their first agricultural foray. Today ITC does a lot of exports through e-choupals. We have to use a mix of technologies to reach rural India and deploy innovative ways of creating business models.

Finally, and most importantly, we need to ensure the vast majority of our population has the requisite skills to avoid a digital divide. In this context, we need a renewed push through both the government’s Gramin Digital Saksharta Abhiyan, and through corporate social responsibility initiatives. A wide array of digital skills need to be mainstreamed into school curriculums especially for first generation school-goers.

Sanjeev is an industry veteran with over 35 years of experience in Strategy, Consulting, Sales, Marketing, Operations in IT and Technology Services. Sanjeev is the CEO and Founder of Strategies2Scale, a consulting firm focused on growth and transformation of start-ups and mid-sized IT & Technology companies. Sanjeev co-founded HCL Comnet (one of the first start-ups in India) and later became President of Industry Verticals as well as the President for Asia Pacific, India and MEA regions at HCL Technologies. In his last corporate role Sanjeev was President of Strategic Initiatives and Global Head of Marketing at Tech Mahindra. Sanjeev has participated in various industry initiatives and forums, notable being:

• Setting up the first fully electronic stock exchange in India, National Stock Exchange of

India (NSE).

• Active participation in liberalization of telecom sector in India-ex President of VSAT

Services Association of India.

• Setting up Distance Learning program at IIT Mumbai.

• Ex-Member of the advisory board on ICT and eco-sustainability for World Economic

Forum.

• Active in IIT alumni and mentor to various start- ups and mid-sized IT services firms in

India and abroad.

• Digital Chair and Visiting Professor for Digital Transformation at School of Inspired

Leadership, Gurgaon

Currently Sanjeev is advising a number of IT firms on sales strategy and digital transformation. Sanjeev is a Mechanical Engineer from IIT, Benares Hindu University (1982) & MBA from Faculty of Management Studies, University of Delhi (1985). Sanjeev loves to coach, mentor & consult and is an active speaker at Industry and Academic forums.

Mitali Nikore, a New Delhi-based economist and Founder of Nikore Associates, an economics research group which raises questions about policies pertaining to a wide range of sectors with an aim to continue questioning policy efficacy and creating better policy design. She is a Development Consultant for the Indian Resident Mission of the Asian Development Bank and a short term Consultant to the World Bank. She also holds the position of Assistant Director at the School of Economics and Commerce, Adamas University. In addition, she is a Global Shaper with the New Delhi Hub of Global Shapers Community, an initiative of the World Economic Forum. She also is a Thought Leader at Centre for Public Leadership’s Fellowship Program. Along with this, she manages and publishes on a regular blog titled “Irrational Economics” as a Columnist with Times of India, and is a regular economics commentator on India Ahead News. Focusing on infrastructure development, industries, MSMEs, and economic corridors, her work spans a wide range of sectors, both in South Asia and Africa, at the national and sub-national level. Mitali has led research inquires on infrastructure financing gaps, gender-based discrimination, framing policy, and programmatic and project-level interventions. She is also a widely published researcher and writer with World SME News, Indian Express, and EPC World.

Leave a comment