“COVID-19 may set back automotive technology by 2-4 quarters”

Rajeev Singh, National Leader and Partner –Automotive, Deloitte India, opines that Covid-19 has compounded the problems of Indian automotive industry. In response, companies may starve R&D funding to sustain core operations, and potentially set back the progress made on alternate fuel and mobility technologies by 2-4 quarters.

TPCI: The last 1.5-2 years have been difficult for the Indian automotive industry. Further the onset of Covid-19 in the country has brought demand to a standstill. How is this expected to impact the industry?

Rajeev Singh (RS): The problems of Indian automotive industry, which has undergone considerable slowdown over the last 12-18 months, were compounded by the onset of COVID-19 due to near-zero demand for vehicles since the lockdown. This downturn in consumer demand has significantly affected auto OEM revenues and cash flows. In response, companies may starve R&D funding to sustain core operations, and potentially set back the progress made on alternate fuel and mobility technologies by 2-4 quarters.

Auto dealers have been unable to deliver vehicles during lockdown, and have reported 30-45 days of finished goods inventory, likely to be heavily discounted post lockdown. Further, with BS-VI sales mandated from 10 days after lockdown ends (and sale of 10% of existing BS-IV inventory until then), dealers face significant burden to liquidate unsold BS-IV inventory worth ~Rs 6,300 crores. Auto-suppliers have a high dependence on migrant labour, whose return to their respective states will further delay revival post lockdown, resulting in a domino effect on the entire value chain. Captive finance companies also face the brunt, as loan defaults will shoot-up, and new loans will drop, given difficulties in determining customers’ creditworthiness, further denting the firms’ profitability. Lastly, the lockdown has put a strain on mobility solutions, used-car, and after-market service providers, many of whose funding depends on aggressive growth projections.

TPCI: One of the consequences of COVID-19 was supply chain disruption. Given that a lot of raw materials for producing vehicles are imported from countries like China, how should the Indian automobile industry move towards the import substitution of these goods? What impact will the paucity of raw materials have on future vehicle prices in India?

RS: The paucity of raw materials gives the Indian auto industry the opportunity to undertake a strategic assessment of supply chain dependencies. The first step would be identification of major components whose supply is critical and work towards identification of means for their indigenous manufacture. The industry needs to adopt new business models that shift costs from fixed to variable, thereby reducing the breakeven volume. This import substitution would lead to increased costs in the short run prior to stabilization.

The industry has already been impacted by the BS-VI transition, but has limited scope for price increase to ensure vehicle demand is not muted. This may mean that major players with deep pockets may be able to make the shift, while smaller players may continue to depend on Chinese raw materials or enter into alliances with other players. In addition, the industry should look at analytics to better monitor the demand-supply gap and design short-term response strategies accordingly.

TPCI: The general understanding is that the fear of being infected with COVID-19 might make the consumers skeptical about new purchases. What can be done to dispel these fears and win back consumer confidence?

RS: The COVID-19 fear will raise challenges in the future and the auto industry has to find innovative solutions to counter them. In the immediate term, OEMs need to adopt hygiene centric process and design changes at consumer touchpoints like dealerships. Each step of the purchase lifecycle (test drives included) would need to be relooked from a hygiene-centric perspective to ensure consumer confidence.

In addition, an omni-channel sales experience (involving virtual sales consultants, remote demonstrations, online sales and digital documentation, usage of VR and live broadcast etc.) helps drive a more “contact-less” retail experience that is expected to become a norm at least in the mid-term. In the long run, OEMs may look to set up partnerships with dealerships, financial service and e-commerce players to design a completely digitalized customer service for sales and aftersales.

TPCI: How long do you expect the automobile industry to take to recover from the demand shock created by Covid-19? What can be done to expedite this recovery?

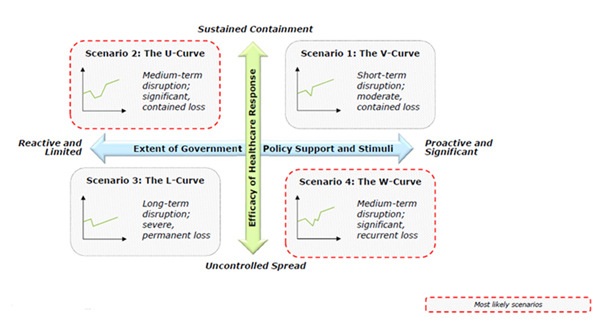

RS: The recovery could most likely materialize in two-ways: U-curve recovery or W-curve recovery, which both involve recovery post medium term disruption in the economy.

U-curve recovery: The U-curve recovery would take place in a scenario of sustained containment but limited and reactive government policy. Movement restrictions would remain stringent until the end of 2020 with varying degrees of relaxation introduced for different businesses. The impact of the pandemic would remain for over two years with tenuous recovery beginning in FY22 and remaining modest through FY23. Pent-up demand would lead revival after mid-FY22.

W-curve recovery: The W-curve recovery would take place in a scenario of uncontrolled spread but proactive and significant policy control and stimuli. Movement restrictions would continue to remain stringent with major hotspots locked down for over two quarters. The first wave of recovery would begin in Q4, FY21 followed by recurrent but less painful bouts of slowdown. Full-fledged and synchronized recovery would be seen from Q3, FY22. Spending would pick up in FY22 driven by pent-up demand recovering to near 2019 levels by mid-FY22.

Regardless of the type of recovery, OEMs would need to take certain steps to expedite this process such as launching smaller/entry level cars to boost demand, designing special financing schemes to mitigate the liquidity crunch, increasing focus on leasing/ subscription options, designing omni-channel sales experience, exploring alternate revenue options, looking for consolidations/ alliances/partnerships and others.

TPCI: Industry insiders are optimistic that the fears of catching the virus and the consequent social distancing might drive up the demand for automobiles in the country. At the same time, rise in unemployment or the shift to work-from-home culture may depress demand. What is your take on the drivers and challenges to demand in the coming months?

RS: In the immediate term, demand for 2W, entry-level 4Ws and pre-owned vehicles could see a spike as customers prioritize ‘personal mobility’ solutions. However, in order to effectively benefit from this expected spike in demand, OEMs would also need to overcome the potential lack of liquidity in consumers owing to anticipated reduction/freezing of salaries both in the public and private sector. Designing special finance schemes, or increasing focus on leasing/subscription options and prioritizing lower cost/trims of models would become important levers for the OEM.

TPCI: How will COVID-19 impact the transition to EVs – demand as well as investments by automotive companies?

RS: The post COVID-19 era will be critical for automotive companies as they are currently witnessing supply chain disruptions and decline in sales. New investments in evolving technologies may take a step back as there will be shift in focus to clear the backlog of inventories and revive the prevailing operations. Moreover, EV manufacturers are expected to face mammoth pressure due to component shortfalls, for which there is heavy reliance on other geographies. There will be limited working capital, which will have to be managed owing to liquidity crises and uncertain demand. Thus, there will be a need for manufacturers to revisit their strategies and alter their investment plans.

Further, the outbreak of pandemic will add restrictions on consumer spending as they might defer discretionary purchases to increase savings. At the same time, consumers are expected to be more concerned about environmental sustainability and may thus be more sensitive towards adoption of green mobility solutions and need for adoption of clean technology like EVs. Hence, the segment could be expected to grow gradually recovering from pandemic and its aftereffects.

Rajeev Singh is a Partner with Deloitte Consulting Practice and leads the Automotive Sector for Deloitte India. He also leads the Strategy & Business Design Practice for Consulting in India. Rajeev has been associated with various committees of SIAM (Society of Indian Automobile Manufacturers), ACMA (Auto Component Manufacturers Association) and is also the co-chair at FICCI on the Industry 4.0 committee. Rajeev brings over 22 years of experience across both Industry & Consulting. His areas of expertise include Market Entry Strategy, New Product Development, Target Operating Model, Business Transformation, Digital Customer Experience and Future of Mobility.

Well put, it was a really interesting take. Thank you for sharing! It is so true, COVID has hit the automobile industry pretty hard. Here’s how automobile has transformed with the COVID crisis. https://www.engati.com/blog/revolutionizing-the-automobi