Reorganising employment structure: The COVID-19 opportunity

India can use the COVID-19 pandemic as an opportunity to correct aberrations in its employment structure and strengthen manufacturing competitiveness in key sectors including electronics, automobiles, auto parts, processed food and beverage, paper, plastics, furniture etc.

- India is an outlier in terms of structural shift in labour employment as it leapfrogged from an agrarian economy to a services economy. Even within the services space, 92% of the workforce is engaged in the unorganised sector with no skill sets, social security or minimum wage frameworks.

- A gradual shift of labour from primary to secondary and then to tertiary brings stability in many macroeconomic parameters like terms of trade, labour productivity, skills, manufacturing competitiveness, economies of scale, etc. As India observed a straight jump from primary to tertiary sector in terms of labour employment structure, our manufacturing competitiveness and capacity to manufacture is still sub-par.

- In the Indian scenario, labour productivity in services is 1.86 (as 32% of labours are adding 59.6% of value in GDP), but this value is only 0.36 in the primary sector. Even though industrial output burgeoned by more than nine times in the last 40 years, employment in the industry went up by two and a half times

- If India aggressively focuses on building mega manufacturing hubs of key products including electronics, automobiles, auto parts, processed food and beverage, paper, plastics, furniture etc, during the COVID phase, we can somewhat bridge the employment structure gap .

Celebrated economist Simon Kuznets received the Nobel prize in economics in 1971 for analysing the employment structure of many economies and linking it with their growth trajectories. His broad findings revealed that the structural shift of labour’s employment from primary sector to secondary and then to tertiary sector is important for any country to follow a stable growth trajectory.

In that sense, India seems to be an outlier in terms of structural shift in labour employment, as it leap-frogged from an agrarian economy to a services economy. The acrimonious fact is that even within the services sector, 92% of the workforce is engaged in the unorganised sector without the requisite skill sets, social security and minimum wage implementations.

While the debate is not new, the question remains relevant. For how long will India reflect and continue with a vacuum in the secondary sector? A gradual shift of labour from primary, to secondary and then to tertiary brings stability in many macroeconomic parameters like terms of trade, labour productivity, skills, manufacturing competitiveness and economies of scale etc. As India observed a straight jump from primary to tertiary sector in terms of labour employment structure, its manufacturing competitiveness and capacity till date is sub-par.

Labourers are moving back towards agriculture from the unorganized service sector, because there is no strong industrial base to buttress employability. This is not the case with developed economies, as their industrial sector is robust in terms of linking primary and tertiary sectors.

Now, let’s compare the share of employment in each sector along with sectoral GDP contribution of few major economies.

Share of labour employment and sectoral contribution to GDP

| Indicators/Economies | USA | Germany | Canada | Japan | Australia | India |

| Share of labour employment in primary sector | 1 | 1 | 1.5 | 3.5 | 3 | 42.2 |

| Share of labour employment in secondary sector | 20 | 27 | 19.5 | 24.5 | 20 | 25.1 |

| Share of labour employment in tertiary sector | 79 | 72 | 79 | 72 | 77 | 32.7 |

| Contribution of primary sector to GDP | 0.95 | 1.3 | 1.9 | 1.5 | 2.1 | 15.4 |

| Contribution of secondary sector to GDP | 18.8 | 26.8 | 23.3 | 29.1 | 25.2 | 24.9 |

| Contribution of tertiary sector to GDP | 77.4 | 71.9 | 74.7 | 69.4 | 72.6 | 59.6 |

Source: Data collected from ILO and World Bank; all figures are in %

From the data provided above in the table, we can surmise that the ratio of sectoral contribution in GDP to its corresponding labour employment as a share in same sector is roughly balanced in the case of all economies except India. For example, in the case of US, labour productivity in the primary, secondary and tertiary sectors is more or less the same (0.95 in primary, 0.94 in secondary and 0.97 in services).

Now, this has many macroeconomic implications to consider. First, there is not much wage gap between the workers in any of the three sectors, thus, keeping labour migration under check. Secondly, terms of trade are majorly balanced. Price realization by selling products/services of all the three sectors is almost the same, which means ability to add value is proportionally comparable. Third, none of the three sectors has pressure to absorb abundant labour due to limited scope in any one of them.

For instance, in India, since manufacturing and services sectors have limited capacity to absorb surplus labour from agriculture, differentials in labour productivity are created, which increase the wage inequality among the three sectors. The fourth aspect is the skill sets, which a labour force gradually learns or adapt while shifting from primary to secondary to tertiary. No labour force can directly be ready to get absorbed in services straightaway from agriculture. Thus, manufacturing or industry acts as the gateway to attain the skills, which have some match with the requirements in services.

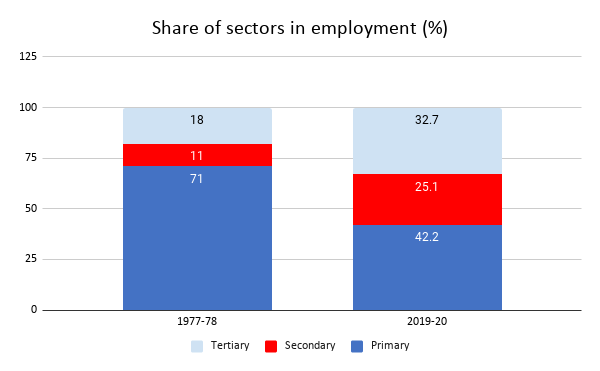

As we can see from the table in the Indian scenario, labour productivity in services is 1.86 (as 32% of labours are adding 59.6% of value in GDP) but in primary sector this value is only 0.36. The situation aggravates even more when we know that the labour force engaged in the primary sector is 42% of the total labour force of the country. As we have mentioned above, labour force engagement shifted from primary to tertiary by missing the manufacturing sector. Let’s have a look at India’s employment structure of past four decades.

Source: NCERT, World Bank

The primary sector continues to be the major employer. Even though industrial output grew by more than nine times in the last 40 years, employment went up by two and a half times. The same applies to the tertiary sector as well. While production in the service sector augmented by 14 times, employment rose by five times. So basically, India’s economy faces certain distortions or aberrations going by the conclusions of economists and researchers like Simon Kuznets. These anomalies have to be corrected only by focussing on growth of industrial base.

Recently we have seen than India has increased its exports of manufactured goods during the COVID pandemic phase. In the past couple of months, India’s exports of finished iron and steel products, manufactured textiles, FMCG products, pharmaceuticals have outperformed many economies. It means if we aggressively focus on manufacturing activities and setting up of mega manufacturing hubs of various products, especially those which will be in great demand including electronics, automobiles, auto parts, processed food and beverage, paper, plastics, furniture etc, during the COVID phase, we can somewhat bridge the gap of employment structure.

This can certainly act as a blessing in disguised. Since India skipped the manufacturing stage, its heavy industries sector is relatively under-developed. Through initiatives to improve infrastructure and ease of doing business, foreign investment in India’s domestic manufacturing sector must be encouraged. Government’s current initiatives to boost infrastructure will facilitate in moving closer towards the goal of becoming a competitive manufacturing hub., which is critical to the goal of becoming a US$ 5 trillion economy.

Leave a comment