Indian economy and COVID 2.0: In anticipation of the rising tide

The second wave of COVID-19 has led to downward revisions in the projections for GDP growth, with rise in infections for rural India an added cause of concern. Consequently, demand revival is important as not all the sectors can be boosted through rising export demand.

- Revisions are being made with agencies downgrading their predictions for FY 2021-22. For example, recently, Moody’s downgraded the GDP growth forecast for India during FY 2021-22 from 13.7% to 9.3%.

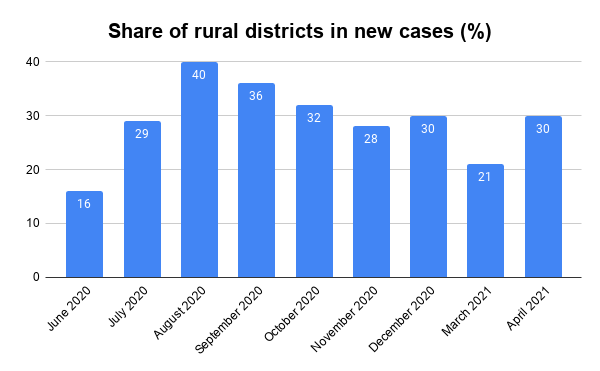

- In the rural sector, the COVID-19 cases are on rise, reaching 30% of the total cases in India in April’ 2021 from 21% in March’ 2021.

- However, growth in trade remains robust due to growing international and domestic demand. Export orders also kept the manufacturing activities up.

- Business activities have slowed down. For the economy to come back on track, a boost to domestic demand is required.

India bore the hit of the second wave of COVID-19 with a daily new number of cases showing an upward trend during whole April’ 2021 till initial days of May’ 2021 (Worldometers data). According to the data released by the Ministry of Health and Family Welfare, states with the highest number of active cases in the country as on 8th June, 2021 are Karnataka (238.9 thousand), Tamil Nadu (232 thousand) and Maharashtra (177.2 thousand).

To prevent the further spread, states have imposed several measures including localised lockdowns, night curfews and a ban on social gatherings. With these restrictions, the economy, which started recovering from the first wave, has yet again been impacted. At the same time, several states have started easing restrictions after fall in daily active cases. For instance, states such as Delhi, Maharashtra, Tamil Nadu and Uttar Pradesh (UP) are gradually allowing opening up of shops, offices, malls with the exception of districts with high number of cases.

During the first year of the pandemic in the country, FY 2020-21, GDP of India contracted by 8%. This year, before the arrival of the second wave, the economy had been expected to be on a strong recovery path with the projections for positive growth in GDP. However, now revisions are being made with agencies downgrading their predictions for FY 2021-22.

Recently, Moody’s downgraded the GDP growth forecast for India during FY 2021-22, from 13.7% to 9.3%. Care Ratings has revised its forecast to 9.2% from 10.2% during FY 2021-22 with the assumption that the lockdowns will be rolled back in June’21. Goldman Sachs’ analysts predict economic activities to be down by 2.9% in April-June 2021 in comparison to January-March 2021, assuming that the restrictions will remain at the current level during April-June’ 2021.

What do the indicators show?

Figures from a CRISIL report show that in the rural sector, the Covid-19 cases are rising, increasing to 30% of the total cases in India in April’ 2021 from 21% in March’ 2021. However, the share is still less than that in August’ 2020.

Source: Wall of worry, CRISIL Report, figures in %

The rise in cases in the rural sector is expected to impact the agriculture sector this time. Arup Mitra, Professor of Economics at Institute of Economic Growth, commented:

“Though agricultural production as such may not be affected, rural non-farm activities will of course be curtailed. Hence, those who used to combine agricultural activities with non-agricultural activities as a matter of livelihood diversification will be hit badly. There are some households which depend on the non-agriculture sector entirely. The opportunities for them have shrunk drastically.”

A look at trade data gives a bright picture for exports, showing robust growth. In May 20201, India’s merchandise exports rose by 67.39% YoY reaching US$ 32.21 billion, while imports grew by 67.45% yoy reaching US$ 38.53 billion. In comparison to May 2019, exports of goods grew by 7.93% implying robust recovery in international demand. However, imports were down by 17.42% in comparison to May 2019 and fell by 18.66% YoY on a sequential basis amid the disruption caused to domestic consumption by the second wave. Exports and imports of merchandise witnessed robust growth of 197.03% and 165.99% YoY respectively during April’2021. This growth in exports has been driven largely by gems and jewellery, petroleum goods and engineering goods.

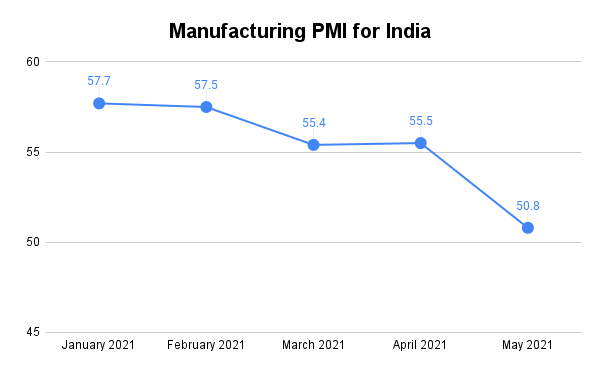

Growth in export demand has also been reflected in the manufacturing sector with activities showing an expansion. In April’ 2021, the IHS Markit India Manufacturing Purchasing Managers’ Index (PMI) was 55.5, a marginal increase over the value of 55.4 in March’ 2021. The index has been above 50 in 2021, albeit higher in the initial two months. Export orders have been rising with April’2021 showing the highest orders for export since October’ 2020. Thus, growth is owed to increasing demand from international markets. However, May’ 2021 experienced a fall in PMI for manufacturing activity to 50.8, saved by export orders. New orders, demand and export orders rose marginally in May 2021. Prices of inputs have contributed negatively with the sharpest rise since mid of 2014, which might be due to higher costs of chemical, plastic, metal, energy, and transportation.

Source: IHS Markit

Situation in the job market

During the second wave, employment has continued to be on a declining path in May, continuing since February 2021. Data from Center for Monitoring Indian Economy (CMIE) reveals that the unemployment rate rose to 11.9% in May 2021 from 7.97% in April, with joblessness prevailing in both urban and rural areas. Discussing the decline in jobs, Professor Parthajit Kayal, Assistant Professor at Madras School of Economics, commented,

Rising unemployment accompanied with a sudden jump in healthcare costs is going to push many informal workers’ families into poverty. This will have a dent on overall consumption in the economy.

Rise in unemployment implies shut down of economic activity and lack of yearning for people to get jobs. This is expected to affect demand significantly. Furthermore, according to Rajeswari Sengupta, Professor at IGIDR, recovery in employment is expected to be slow due to fear among people for the 3rd or 4th wave of coronavirus along with delay in vaccination.

Impact on business activities

Overall, business and commercial activities have slowed down during the second wave in the short term. Nomura India Business Resumption Index (NIBRI) dropped to 60 for the week ended May 23 from 61.9 in the week ended May 16. The index has been gradually falling with its value equal to 64.5 for the week ended on May 9. However, in the consecutive weeks the index showed improvement, reaching 69.7 in the week ending June 6, 2021, implying business activities were worst hit in the month of May.

Some of the industries facing the negative brunt are aviation industry, tourism and automobiles. Demand in the tourism sector has again declined with regions such as Kashmir and Kumarakaon reporting less number of visitors and cancellation of bookings.

Another sufferer, the domestic aviation sector experienced -38.13% year over year (yoy) and 36.71% month over month (MoM) growth in number of passengers during Jan-Feb, 2021, shows the latest statistics. CAPA India opines that the second wave of Covid-19 can lead to a fall down of domestic aviation industry. Consolidation in the sector is now unavoidable, which would result in only 2-3 airlines operating in the economy.

Automobiles have been hit with the fall in demand amid a surge in the number of cases. For instance, in April’ 2021, for passenger vehicles (PV), Maruti Suzuki witnessed 7% MoM drop in sales and Hyundai’s sales drop by 6.8% MoM.

For some other businesses, however, impact has been lenient. For instance, construction activities are expected to be resilient at large with the credit profile for companies expected to be unaffected by the resurgence of cases, said ICRA. Resilience is expected to be higher for work in the remote areas. However, activities in the urban areas such as construction for metro rail are expected to be affected due to localized lock downs and reverse migration of labor.

Further expectations

To look at the possible impact of the second wave on the economy, CRISIL looked at the advanced economies (such as Germany, US and UK) which have gone through their second or third wave. It showed the economic impact has been less in the countries as people got habitual to live with the pandemic. Furthermore, vaccine roll out led to increase in mobility in markets such as the US and the UK, where more than 40% of the population has been vaccinated. Manufacturing activities also continued to expand in the first quarter of 2021 in these economies.

In the Indian economy, demand revival is important as not all the sectors can be boosted through rising export demand. Prof. Mitra commented that production in India need to be improved along with creation of employment opportunities. Mechanisation can expose the economy to the risk of job-less growth. RBI’s recent measures have been focused to provide support to the health care sector and worse affected businesses. Nevertheless, recovery for the economy is still directly linked with the trend in the number of COVID-19 cases and the progress of the vaccination drive.

Leave a comment