Electronics Manufacturing Policy: India Should Move Beyond Self-Reliance

Dr Sunitha Raju asserts that while India has the capability to integrate with global value chains in electronics, the focus should be on building a strong component ecosystem, incentivizing value addition over imports, developing indigenous standards and promoting SMEs.

Electronics manufacturing is one of the fastest growing industries in the world. With wide applications across industries, India’s demand for electronics and components has been growing over the last decade, led by a growing economy, higher disposable incomes, rising middle class and evolving technologies. The country’s demand is projected at US$ 400 billion by 2025 (NPE, 2019). The importance of this industry is also significant from the employment perspective. The NSDC has estimated a growth in employment from 4.33 million in 2013 to 8.94 million in 2022 if impetus is given to domestic manufacturing (NSDC, 2018).

Global electronics industry is valued at US$ 2 trillion out of which, Indian exports stand at US$ 3.1 billion in 2017-18, i.e. is less than 1 per cent. Similarly, India’s share in world electronics hardware production is about 1.5% (NITI Aayog, 2016). On the domestic front, the demand is projected at US$ 400 billion by 2025, domestic manufacturing (supply) was at US$ 53 billion in 2017-18 (NPE 2019). If we fail to bridge this demand-supply gap, the natural fallout is an increasing and unsustainable dependence on imports. The trade balance in the electronics sector has already deteriorated from

Chart 1

Source: Authors calculation from WITS database

US$ – 0.99 billion in 2000 to US$ -19.1 billion in 2017 (see Chart 1). If not addressed, electronics could emerge as the highest import item, even outpacing oil imports.

Under this compelling situation, the Government of India has shown the right intent towards making India self-reliant in the electronics sector; be it through the National Policy on Electronics (NPE), 2012, NPE 2019 and the recently announced initiatives like Production Linked Incentive Scheme (PLI) for Large Scale Electronics Manufacturing, Scheme for Promotion of Manufacturing of Electronic Components and Semiconductors (SPECS) and Modified Electronics Manufacturing Clusters (EMC 2.0) Scheme.

These initiatives gain significance considering the extremely dynamic nature of the industry, its growing importance in global trade and the continuing rise of new technologies like AI, IoT, robotics, etc. The importance of these policies can be gauged by taking a quick look at the composition of the imports of electronics and the trends that have driven them.

Persistent import dependence

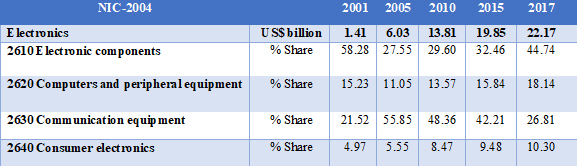

Electronics have applications across many industries. As per the NIC classification, electronics manufacturing has four broad segments, viz. Electronic components & Semiconductor design (2610), Computers and peripheral equipment (2620), Communication equipment (2630), and Consumer electronics (2640). The import trend of total electronics and its segments is presented in Table 1. The total electronics import was US$ 1.41 billion in 2001 and it has increased to US$ 22.17 billion in 2017, with a CAGR of 7 per cent from 2010 to 2017.

Trend in imports of Electronics Products

Source: Author’s calculation from WITS database

In 2001, the share of the Electronics components was the highest at 58%, followed by Communications equipment at 22%. While the significance of these two sectors continued in 2017, the relative share of Consumer electronics increased from 5% to 10.3% during this period. In absolute value, Consumer electronics increased from US$ 0.07 billion in 2001 to US$ 2.28 billion in 2017. The rise in imports of electronic components, consumer electronics and computers & equipment is particularly significant from 2010 onwards, thereby highlighting the need to understand the underlying factors. It may be underlined that many policy initiatives in the early 2000s have directly or indirectly impacted the domestic manufacturing capability of the electronics industry.

First, under the Information Technology Agreement (ITA-1), India was obliged to reduce the duties and other charges in four stages from 1997 to 2000 for 165 HS products. However, under the Special and Differential treatment, India was allowed to reduce the tariffs to zero by 2005. It is pertinent to underline that the base tariff of 66.4% in 1996 was brought down to zero by 2005. The correspondence between the rising imports of electronics from 2005 is clearly evident in the above Table 1. The rise in imports of components is particularly significant. The value of imports of components increased from US$ 0.82 billion in 2001 to US$ 9.92 billion in 2017. The share of China increased from 7% in 2001 to 62% in 2017. The same trend can be observed in Consumer Electronics (2640) as well.

Second, combined with ITA-1, the FTAs with ASEAN and S Korea have contributed to a surge in imports of non-ITA products, particularly considering the highly competitive electronics industry in these countries. Under the CEPA with Korea, 8 non-ITA products were made duty free in 2010, 60 tariff lines were made duty free in 2014 and 277 tariff lines were made duty free in 2016. Subsequently, the rise in imports of Computer equipment (2620) is reflected in the increase in share from 0.41% in 2010 to 8.96% in 2017. In the case of Communication equipment (2640), the share of ASEAN and Korea increased significantly post-2010.

One of the concern areas in this regard is the inverted duty structure wherein higher duty is imposed on components and parts and lower duty on final products. The natural outcome is the imports of final goods instead of components. The experience of imports of mobile phones underlines this trend. In 2014, the mobile phones imports from China and S Korea was US$ 6.3 billion. However, under the Make In India Programme, Chinese and South Korean companies set up production facilities in India.

While the imports of mobile phones decreased to US$ 3.3 billion in 2017, the import of parts of mobile phones and telecom equipment increased from US$ 1.3 billion in 2014 to US$ 9.4 billion in 2017. As such, local assembly of goods has been incentivized in the absence of sufficiently developed domestic parts and components supply base.

Third, the FDI inflow into electronics manufacturing has not actually picked up. Between 2000 and 2015, electronics manufacturing received only 0.66% of the total FDI inflows (NITI Aayog, 2016). This clearly underlines the limited incentives for large foreign original equipment manufacturers (OEMs) to invest in local production and only focused on final assembly plants in India. Therefore, it is not surprising that the value addition in electronics manufacturing is less than 15% in India.

The development trajectory of the electronics industry in China, South Korea and Taiwan focused on upgrading production and skill development within the framework of vertical industrial development strategy. This involved incentivizing productivity enhancement, promoting backward linkages and technology spillovers between foreign enterprises and domestic firms. With strong correspondence between trade and industrial policies, this has resulted in promoting R&D, design and manufacturing capabilities.

Particularly important is China’s aggressive policies on technology transfer through joint ventures while at the same time promoting the indigenous technology capability. As such, China emerged as the world’s largest producer of electronics. Similar policy frameworks are being adopted by Vietnam and Thailand. As against this, while India has developed design capabilities in IC (Integrated Circuits), largely confined to the MNCs R&D divisions, the translation of the same to Indian domestic manufactures has been virtually absent leading to a fractured supply chain base for components.

If India has to emerge as a dominant player like China and South Korea, it needs to have the design capability coupled with manufacturing resilience and a developed tooling industry. Particularly with high rate of obsolescence and evolving technology in this industry, the investment climate needs to be conducive. Further, integration of the SME through cluster development with appropriate technology support can result in cost benefits of agglomeration and scale economies. While the large domestic market can provide the impetus for large scale production and the associated efficiency gains, the focus should be on developing export competitiveness, which can catapult this important industry into high value addition production. In this regard, the FTAs (existing and new) should provide opportunities for integrating into global value chains, particularly in the Asian region.

Policy Initiatives

The recent policy announcements of implementing three new schemes for electronic industry need to be viewed from the perspective outlined above.

The Production Linked Incentive Scheme (PLI) for large scale electronics manufacturing focuses on mobiles and specified electronic components. Considering that the components account for 70-80% of the cost of the final product, incentivizing component production in India can promote design capability along with competitive manufacturing process. Given that the current manufacturing activities in India are mainly in contract manufacturing, assembling and packaging, the PLI provides incentives for promoting domestic production and investment. The scheme provides incentives of 4-6% of sales above the base year (2019-20) threshold with minimum investment requirement.

The threshold sales and investment requirement differs between foreign and domestic companies thereby targeting MNCs to establish component production facilities in India. As the threshold new investment covers R&D, transfer of technology, plant and machinery, the scheme aims at upgrading the technological processes in component manufacturing. This will promote contract manufacture of chip makers (memory chips, microprocessors, commodity integrated circuit, complex system on chips), which over time can develop competence for design and development activities. With the mandatory investment requirement, the domestic value addition can increase over time.

The Scheme for Promotion of Manufacturing Electronic Components and Semiconductors (SPECS) is aimed at offsetting the disability for domestic manufacturers of components and semiconductors. It is applicable for investments in new units or modernization/expansion of capacity of existing units. The scheme provides 25% of capital expenditure for both domestic and imported goods and covers products largely falling under passive, active components and semiconductor and fabrication goods. The minimum threshold investment eligible for the scheme ranges from Rs 5 crore to Rs 1,000 crore; thereby covering the entire production process of manufacturing even while recognizing that the technological process required is not the same across all components.

The Scheme for Modified Electronics Manufacturing Clusters (EMC 2.0) aims at upgrading common technical infrastructure and providing common facilities for the ESDM units. The scheme provides financial assistance for developing clusters for efficient supply chain.

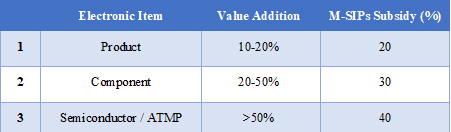

Together, the above schemes provide a holistic framework for developing an appropriate electronics manufacturing ecosystem in India. Whether India can emerge as an electronics manufacturing hub would depend on the implementation of these schemes. A regular evaluation of the mandated outcomes need to be carried out for corrective measures to be implemented. The existing M-SIP can be modified to target the SMEs in this industry. As such, the threshold investment can be reduced from the current Rs 10 crore to Rs 5 crore. Further, to link incentives with productivity enhancement, capex subsidy should differentiate between high and low value-added activities. As such, the following can be considered:

From a long-term perspective, the correspondence between industry and trade policies needs to be maintained. For export promotion, deemed export and MEIS benefit of 7% for locally manufactured PCB exports can be considered. Similarly, for products facing inverted duty structure, duty on components can be reduced to zero or on par with final product. The denial of input tax credit in GST on import of finished equipment may be reviewed.

Further, domestic standards have to be developed and efforts made for international recognition. This is necessary for not only ensuring requisite quality for imports but also to subject exports to international quality standards.

Dr. Sunitha Raju is a Professor at IIFT. She has 30 years of extensive experience in Education, Research, Policy formulation and Evaluation and held the positions of Chairperson (ICCD), Chairperson (Research) and Chairperson (GSD). Her areas of expertise include Trade Policy Formulation & Evaluation, Trade modelling, Agricultural Policy Analysis, WTO rules & Regulatory framework, Free Trade Agreements, Survey Research, Performance Reviews, Training & Management Development Programmes.

Leave a comment