Commercial realty: Down, but not out

The COVID-19 induced lockdown posed key questions for the commercial realty space, particularly with concerns that work from home (WFH) may become a more permanent phenomenon, at least in part. IT/ITeS, the major contributor to office space, led the debate, and a number of companies in fact indicated that they could continue with the practice for a longer period.

On the other hand, social distancing norms could also indicate that companies would be compelled to deploy ‘less efficiency’ in office space design when it came to seating arrangements. Experts are relatively confident that the office space will not go anywhere too soon due to an odd crisis in 2021. The following charts give an overview of the immediate impact of COVID-19 and the lockdown on commercial office spaces, warehousing and hospitality sectors in India.

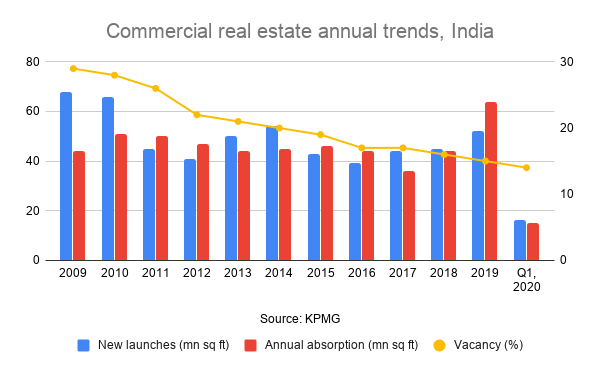

Record absorptions preceded COVID-19 induced slowdown

Commercial realty faced a chronic oversupply situation post the Global Financial Crisis (GFC) with high vacancy levels persisting for 2-3 years. Regulatory changes by RERA, real estate investment trusts (REIT), and GST regime, coupled with long term contracts, have led to steady cash flow models and fairly stable return levels. In 2018, commercial realty attracted around 60% of total investments in the real estate sector, replacing residential as the major investment source.

Interestingly, the COVID-19 induced lockdown follows a year of record absorptions in the commercial realty sector. Annual absorption in 2019 was at 64 million sq ft compared to new launches at 52 million sq ft.

Warehousing anticipates quicker recovery

Warehousing sector has shown strong traction in recent years, primarily led by 3 PL companies and e-commerce firms due to consolidation and upgradation to modern facilities. Government reforms like “Make in India”, GST implementation etc, have increased uptake from manufacturing companies. The warehousing sector has seen investments exceeding US$ 200 million in 2019.

Demand for warehousing space could drop due to impact on 3 PL, FMCG, retail and manufacturing segments. However, e-commerce and essential products supplies have limited the negative impact, and are also expected to boost recovery.

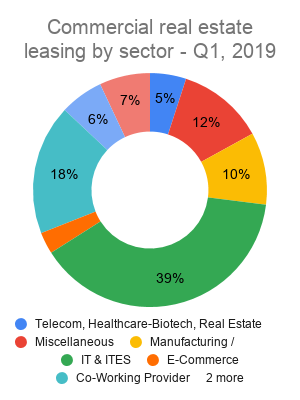

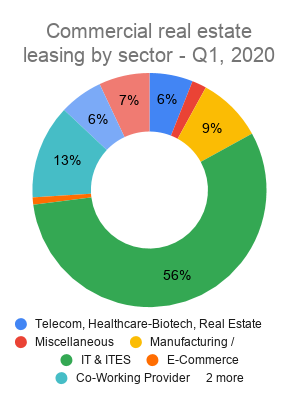

Share of IT/ITeS grows

IT/ITeS occupied around 39% of new office leasing activity in Q1, 2019. In Q1, 2020, its share had grown to 56%. The share of co-working spaces declined from 18% to 13%, e-commerce dropped from 3% to 1%, while share of BFSI remained stable at 7%.

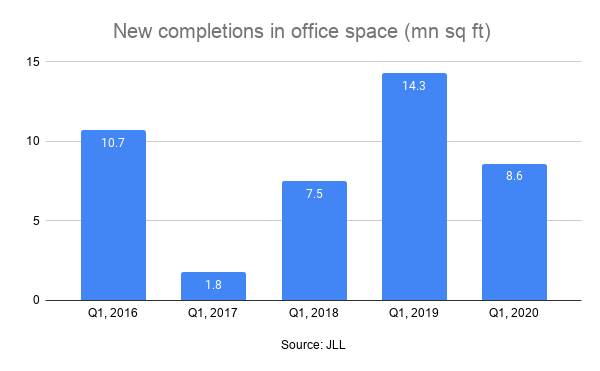

New completions witness sharp drop

New completions in the office space witnessed a sharp drop by 40% YoY to reach 8.6 million sq ft in Q1, 2020. This is the second largest drop in the past 5 years, and reflects the impact of major disruptions due to the COVID-19 pandemic and subsequent lockdown. Bengaluru and Delhi-NCR grabbed around 60% share of new completions in Q1, 2020. On the other hand, vacancies remained range-bound, dropping slightly from 13.3% in Q1, 2019 to 12.8% in Q2, 2020. However, vacancy levels dropped to low single digits in prime business submarkets.

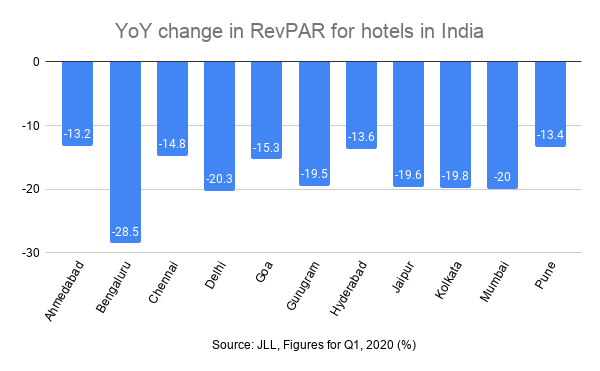

Severe impact on hotels RevPAR

Hotels showed a strong drop in Revenue Per Available Room (RevPAR) in Q1, 2020, as the lockdown has totally shut out all forms of travel. Mumbai remained the largest contributor to RevPAR, desite a 20% YoY decline. The drop was strongest for Bengaluru at 28.5% YoY. Until a strong flattening of the COVID-19 curve or development of a permanent cure, the prospects for the hotel industry are considered quite weak as consumers are expected to stay wary of all kinds of non-essential travel.

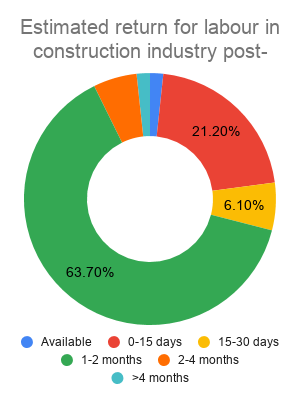

Migrants weaken supply side

India has an estimated 139 million internal migrants, and around 35% of them work in the construction sector, with the biggest source states being UP and Bihar. As the lockdown brought them face-to-face with an immediate loss in livelihood and uncertain future, thousands of migrants looked to return to their hometowns.

Recovery in the supply side for commercial realty is highly contingent on the return of migrant labourers to cities. Around 63.7% of respondents in a JLL survey of leading contractors and suppliers feel that that labour will be able to return in 1-2 months. Interestingly, around 43% of respondents also felt that the chances of workforce in labour camps returning to their home town is quite high post-lockdown.

Leave a comment