Breaking the complex juggernaut of the cashew sector

• Cashew industry of India has traditionally held an oligopoly in the global cashew kernel sector primarily because of the processing infrastructure and capacity.

• India imported 834,326 MT of raw cashew from world primarily Cote D’ Ivoire, Benin, Ghana and Guniea in 2018-19, as per Ministry of Commerce & Industry

• Dependence on imported raw cashew by processing units in India is prominent even in the higher end of the value chain of cashew, for example roasted/salted cashew or cashew butter.

• Devising a policy which reduces imports by accounting for the difference in harvest season between India and Africa will be in the interest of processors as well as growers.

Cashew is one of the most demanded dry fruits across the globe. As per the International Nut and Dried Fruit council foundation the cashew consumption per capita in 2017 is estimated to be as high as 0.106 kg per capita on cashew kernel basis in the world. The top producers of cashew in the world are India, Cote d’ ivore, Vietnam and Tanzania.

The cashew industry of India has traditionally held an oligopoly in the global cashew kernel sector primarily because of the processing infrastructure and capacity to process raw cashew to cashew kernels in India. The other key competitor is Vietnam in processing the kernels from raw cashew. As per International Trade Centre (ITC), the processing capacity of India is 235% of the domestic cashew production, while it is 200% for Vietnam.

Now the question arises who feeds in the 135% and 100% to the processing facilities in India and Vietnam respectively? It is here that Africa comes into the picture. The major producers of cashew are Cote d’ Ivore, Guinea, Benin, Ghana, Nigeria, Burkina Faso, Tanzania, Mozambique and Kenya in the African region.

India imported 834,326 MT of raw cashew from world primarily Cote D’ Ivoire, Benin, Ghana and Guniea in 2018-19 according to Ministry of Commerce & Industry. As per the Directorate of Cashew Nut & Cocoa Development (DCCD), India produced 817,000 MT of cashew in 2017-18. Hence there was a shortfall of approximately 800,000 MT of raw cashew in 2018-19 which was met through imports.

India’s import of Raw Cashew in 2018-19

| From | In mn US$ | In MT – Quantity |

| World | 1,566.68 | 834,326.63 |

| Top 3 exporters | ||

| BENIN | 284.32 | 140,041.47 |

| COTE D’ IVOIRE | 344.36 | 190,708.91 |

| GHANA | 192.81 | 101,334.87 |

Source: Ministry of Commerce & Industry

India’s import of Cashew Kernels in 2018-19

| From | In Mn US$ | In MTs-Quantity |

| World | 40.86 | 5,309.80 |

| Top 3 exporters | ||

| VIETNAM | 29.12 | 3,658.90 |

| COTE D’ IVOIRE | 3.68 | 630.20 |

| UAE | 2.18 | 334.43 |

Source: Ministry of Commerce & Industry

Production wise data of cashew in India in 2017-18

| State | Area (‘000 ha) | Production (‘000 MT) | Productivity (kg/ha) |

| Kerala | 92.81 | 88.18 | 962 |

| Karnataka | 129.06 | 89.447 | 672 |

| Goa | 58.25 | 34.259 | 561 |

| Maharashtra | 191.45 | 269.44 | 1378 |

| Tamil Nadu | 142.27 | 71.03 | 478 |

| Andhra Pradesh | 186.78 | 116.915 | 600 |

| Odisha | 193.98 | 98.585 | 513 |

| West Bengal | 11.36 | 12.96 | 1140 |

| Jharkhand | 14.83 | 6.13 | 393 |

| Chhattisgarh | 13.7 | 9.83 | 681 |

| Gujarat | 7.25 | 6.5 | 900 |

| Pondicherry | 5 | 2.16 | 432 |

| Assam | 1.05 | 1.13 | 1028 |

| Tripura | 4.25 | 3.45 | 812 |

| Meghalaya | 8.58 | 6.12 | 686 |

| Manipur | 0.9 | 0.324 | 360 |

| Nagaland | 0.5 | 0.54 | 1080 |

| Total | 1062.04 | 817 | 753 |

Source: Directorate of Cashew Nut & Cocoa Development (DCCD)

The dependence of imported raw cashew to processing units in India even in the further value chain of cashew for example roasted/salted cashew or cashew butter too is high primarily because of the production demand mismatch as discussed earlier.

An overview of the duty and other policies, i.e. the import duty on raw cashew is 2.5% and duty on cashew kernels is 70%, other restrictions such as Minimum Import Price of Rs 720/680 on whole/broken cashew kernels imported in India show that policy and duty structure is in tandem with the industry. However the industry is facing an acute crisis. Why?

There are three major reasons to it- First is the cost of processing raw cashew to kernel is very high in India as compared to Vietnam, the other competitor. The only respite is with regard to the quality of the kernels processed in India, since the processing is primarily manual and hence commands a premium in the international market. Second is the cost of production of raw cashew – as compared to African countries such as Benin, the cost of producing raw cashew is much higher in India. As per industry inputs, the difference in cost may be estimated to be approximately 40-50%. However as per industry inputs as well as ITC’s report, since India and Vietnam are the key markets for raw cashew, the production in these countries determines the global prices of cashew. Additionally, the existence of a number of intermediaries in the African cashew market is the other reason for the high cost, as it may even be lower in African markets in their absence. The third is the demand for cheap cashew kernels by the processing units involved in further value addition for example- roasted/salted/butter cashew etc.

As evident, there exists a resistance among the domestic growers regarding the import of either kernels or raw cashew. Processors want to be allowed to procure cashew kernels at the most competitive rates and demand a favourable policy structure to import raw cashew. Kernel growers demand a complete ban on import of kernels.

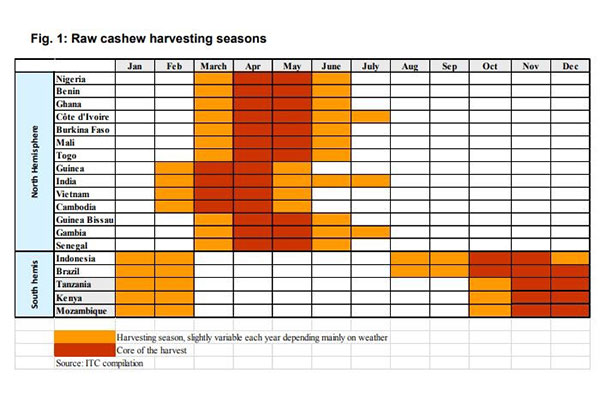

The panacea to this Pandora’s box lies in tapping the difference in the harvest cycle of East Africa and India. The sowing and harvesting cycle of cashew in Africa is different than India as shown in the chart below April-May for India and Nov-Dec for East Africa. One key attribute of cashew that strengthens the case for promotion of domestic cashew cultivation in a larger area, despite comparatively low productivity in India is that the cashew tree plays an important role in maintaining the ecological balance of the dry regions and is instrumental in arresting soil erosion. It can be grown on agriculturally unsuitable land as well. The cashew tree is multi-functional i.e. apart from producing cashew nuts; it supplies timber, firewood, medicines, fodder, etc. as well.

Devising a policy which accounts for the said difference in harvest season will cater to both the stakeholders i.e. processors as well as growers. The idea is to restrict import of all types of cashew in India during April to May i.e. the harvest month of Indian cashew; thus the growers will be able to sell their produce at good margin. Similarly the processors may continue to import in rest of the period as per the processing capacity of the units so that the situation of running at below capacity may be averted. Additionally, greater policy emphasis must be laid on processing cashew apple, husk and producing processed cashew products like jams, pickles, juices and anacardic acid to supplement cashew growers’ income.

Leave a comment